In this blog post, we discuss how cryptocurrencies are good for momentum-based trading. Small-cap tokens, in particular, have violent, volatile, short lives. Based on these principles, we present a profitable trading strategy by constructing a portfolio of tokens based on their all-time high prices. The strategy is now available for you to use in a DeFi vault.

Today, you can use this strategy yourself here.

Buy tokens that go up and up only

Our thesis about the cryptocurrency markets are

- Cryptocurrencies are momentum-driven.

- Most cryptocurrencies will go up only once, if ever: the failure rate is high, the success rate is low, and after a token starts going down, the token rarely comes up again.

- The momentum theses: If it went up yesterday, it will likely go up today.

Based on the theses above, we design a trading idea

- Buy tokens that go up.

- Buy tokens that have been going up: This can be determined by checking if the token's price is above its (local) all-time high.

We also will find out that:

- Tokens go up only for short periods; cryptocurrencies trade sideways or down most of the time. Most tokens go to zero over a longer period, so any long-term index portfolio holding tokens makes little sense.

- Most of the tokens go up simultaneously; thus, if you want to buy tokens that go up, you have a lot of idle cash between the periods when all tokens go up.

- In small-cap markets, the life cycle of the token is short; new tokens enter the markets weekly, requiring an open-ended trading universe.

- The small-cap markets are constrained by the available liquidity (market depth, TVL). You must size your positions very small to avoid excessive price impact.

Based on these ideas and observations, we create simple strategy rules:

- Create a portfolio of tokens above their (local) all-time high.

- Weight and manage risk accordingly based on the available liquidity.

The strategy has now been released: All-time high strategy. We have deployed the first iteration of this strategy on the Base L2 blockchain, other chains will follow shortly.

How can you use this trading strategy?

The strategy described is deployed today as a Lagoon vault on the Base blockchain. Having the strategy deployed as a vault allows third parties to deploy capital there easily while still maintaining self-custodial control over their assets.

As a user, you can use the strategy by depositing and redeeming your tokens in the strategy vault, as with any decentralised finance vault. The vault uses the ERC-7540 standard: deposits and withdrawals are processed in four hours.

The benefits of the onchain, self-custodial strategy include:

- Self-custodial: You are always in control of your assets, ensuring that there is no counterparty risk you could not withdraw, as, for example, what happened with FTX.

- Transparency: You always know what has happened and what will happen, eliminating any possibility of deception.

- Easy onboarding: Because of its onchain nature, users can directly deposit smart contracts into the strategy vault from their cryptocurrency wallets; no creation of user accounts or API keys is needed.

- Composable: The strategy can utilise several DeFi protocols and is not limited to taking trading positions. More about this later.

How the strategy works

This strategy is fully transparent for users. Here is the explanation of the logic of the strategy.

The strategy has trading rules to rebalance the portfolio of tokens based on the "signal", which is the distance of the current price from the all-time price.

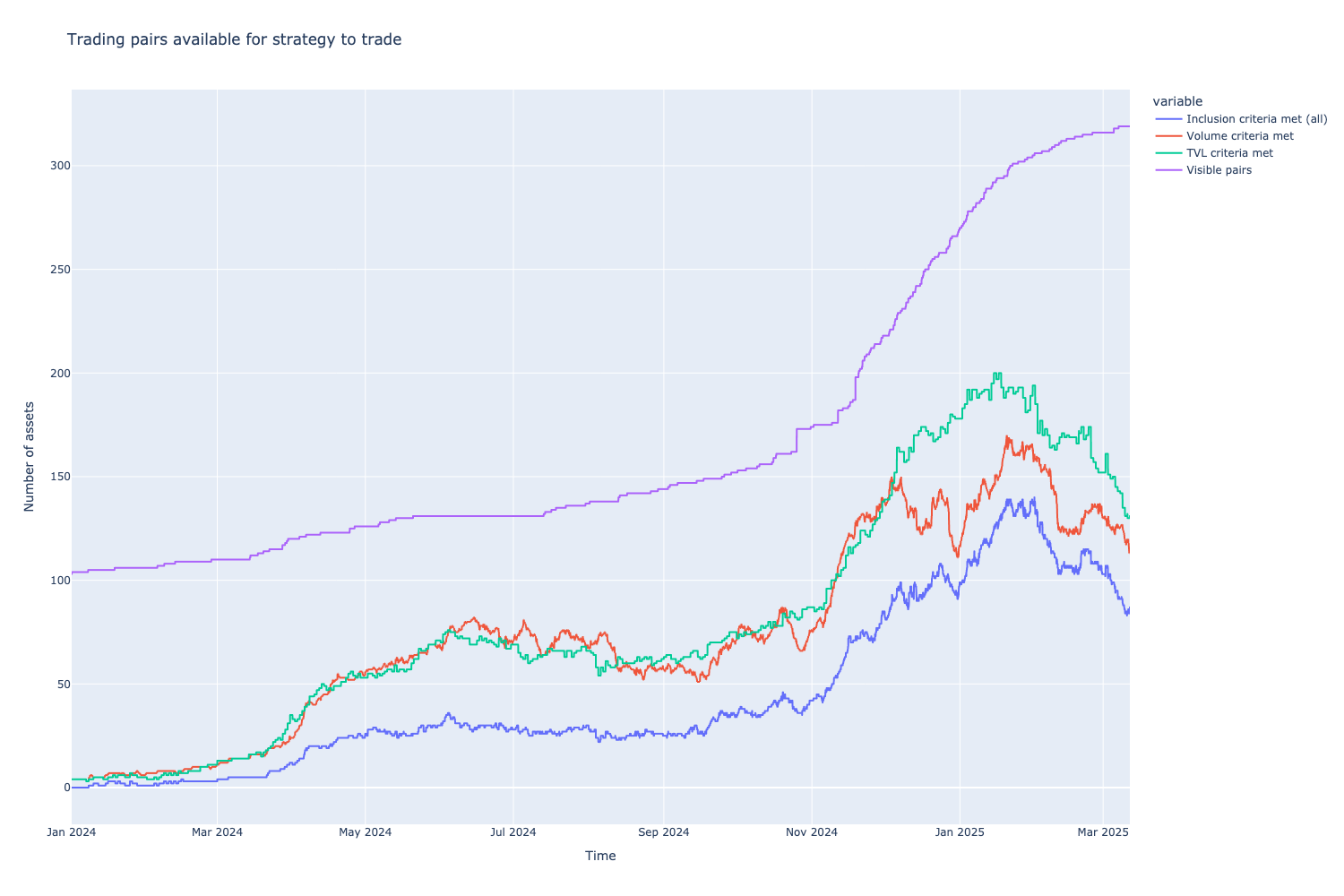

- The strategy trades an open-ended trading universe and includes Uniswap v2 and v3 trading pairs on the Base L2 blockchain, fulfilling minimum volume and TVL thresholds.

- The signal is how much the current price is above the long-term all-time high. This is a continuous trading signal, with no discrete enter/exit step. In an ideal scenario, we start to slowly enter the position and buy the token when the price increases (the signal gets stronger) and then exit the position when the token reaches its all-time high price.

- The signal is filtered using RSI to get rid of some edge cases.

- The strategy constructs a portfolio by rebalancing the tokens where this signal is above the threshold every hour hours.

Here is the core signal logic. You can find the full backtesting notebook here.

The threshold values are chosen through a static optimisation process. The same parameters were tested in different markets to avoid overfitting and sample bias. While the performance was not as good, the strategy still outperformed BTC and ETH. Later, we plan to make these parameters automatically adapt through continuous learning.

Utilising idle cash in decentralised finance

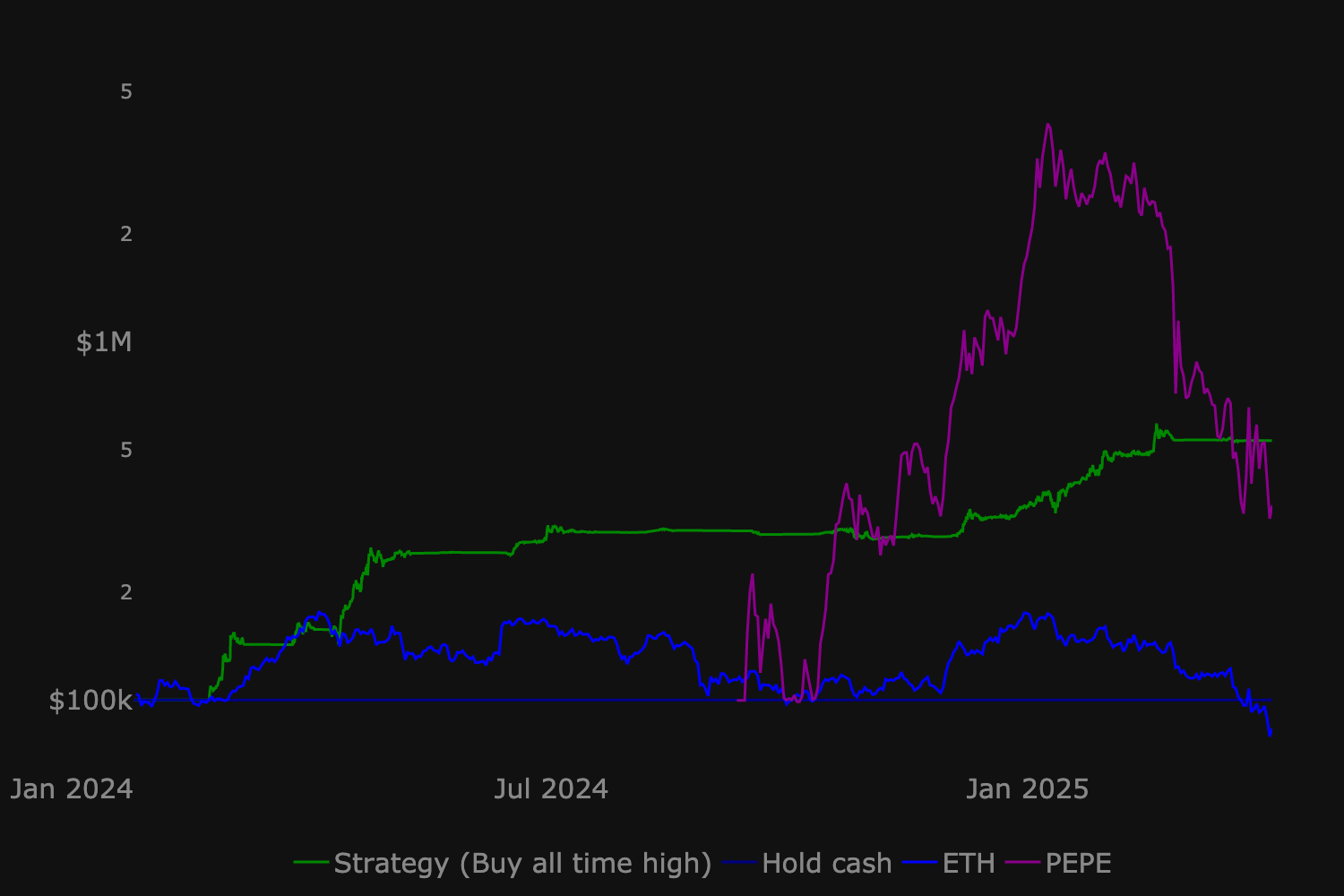

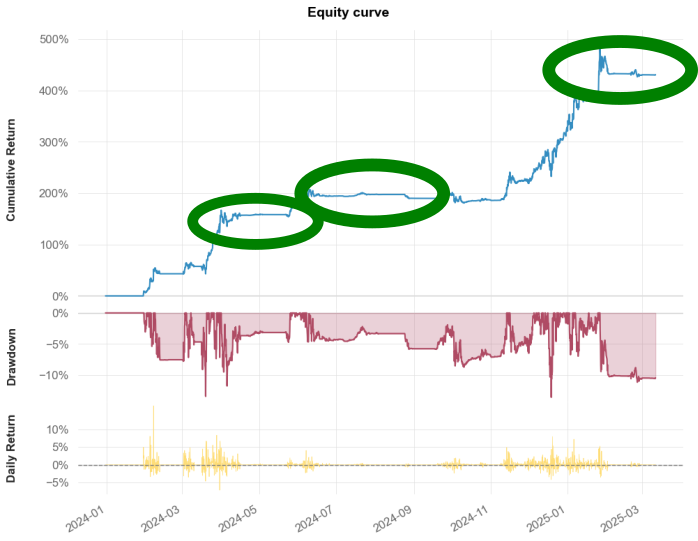

If you look at the strategy equity curve, you can see this kind of strategy captures a lot of upside during the violent upside cycles but stays out of the markets most of the time. This makes sense because often gains are only made on a few days every year, during so called bull-run.

Because the period of interesting price action is limited, the strategy ends up sitting on idle cash. This would not be capital efficient, as we are losing the opportunity to earn interest on that money.

Enter decentralised finance. In decentralised finance, we can easily compose various protocols, vaults, and other financial primitives together, as they are all open and on the same ledger. We can move from a directional position ("holding a token going up") to an interest-earning position ("yield farming") in a single blockchain transaction, without missing yield for a beat. This sort of strategy mixing and efficiency is not possible in traditional finance or centralised exchange trading strategies.

- When cryptocurrencies go up ("bull market"), buy cryptocurrencies.

- When cryptocurrency markets are slowed down ("crab market") or going down ("bear market"), we enter a yield farming position.

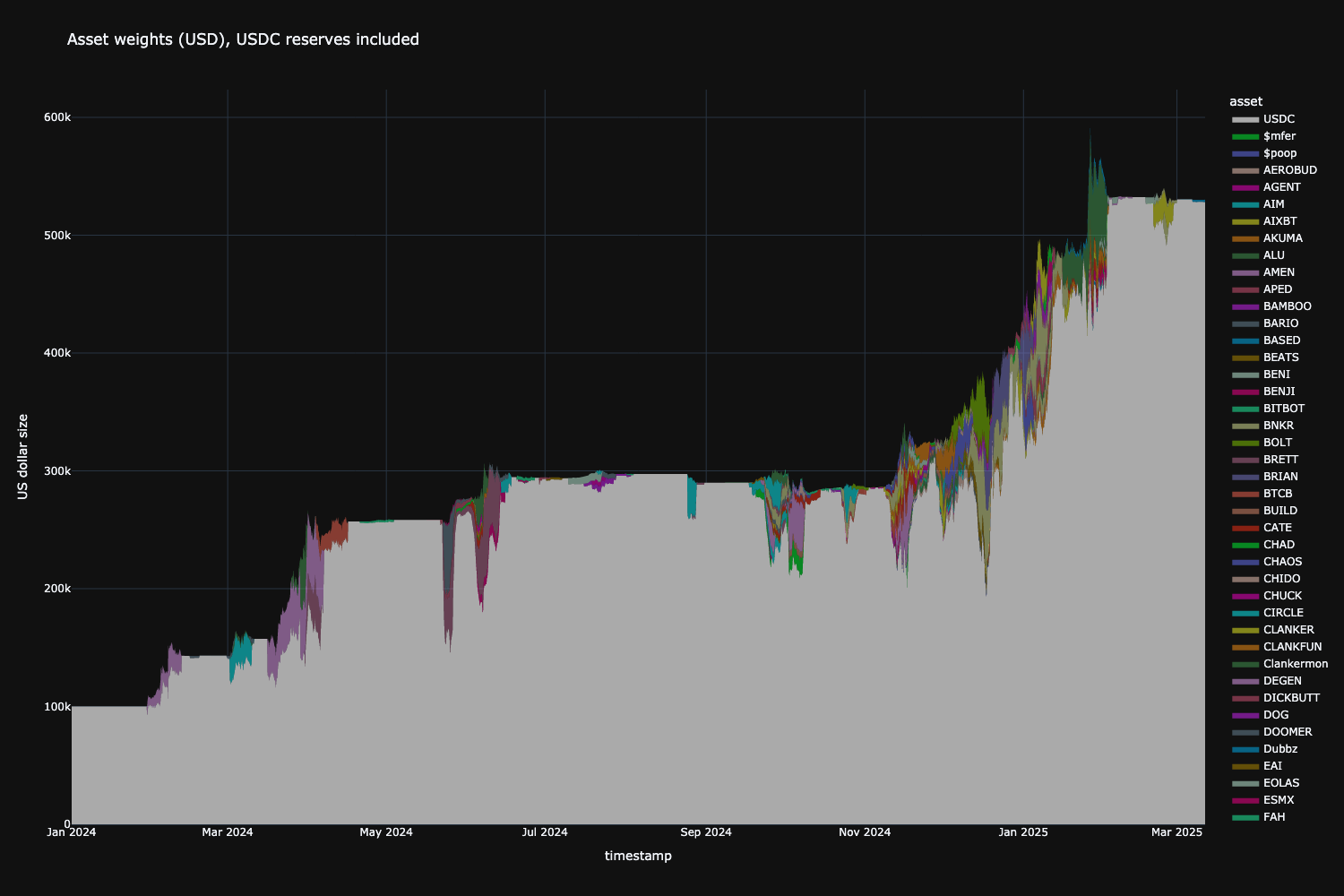

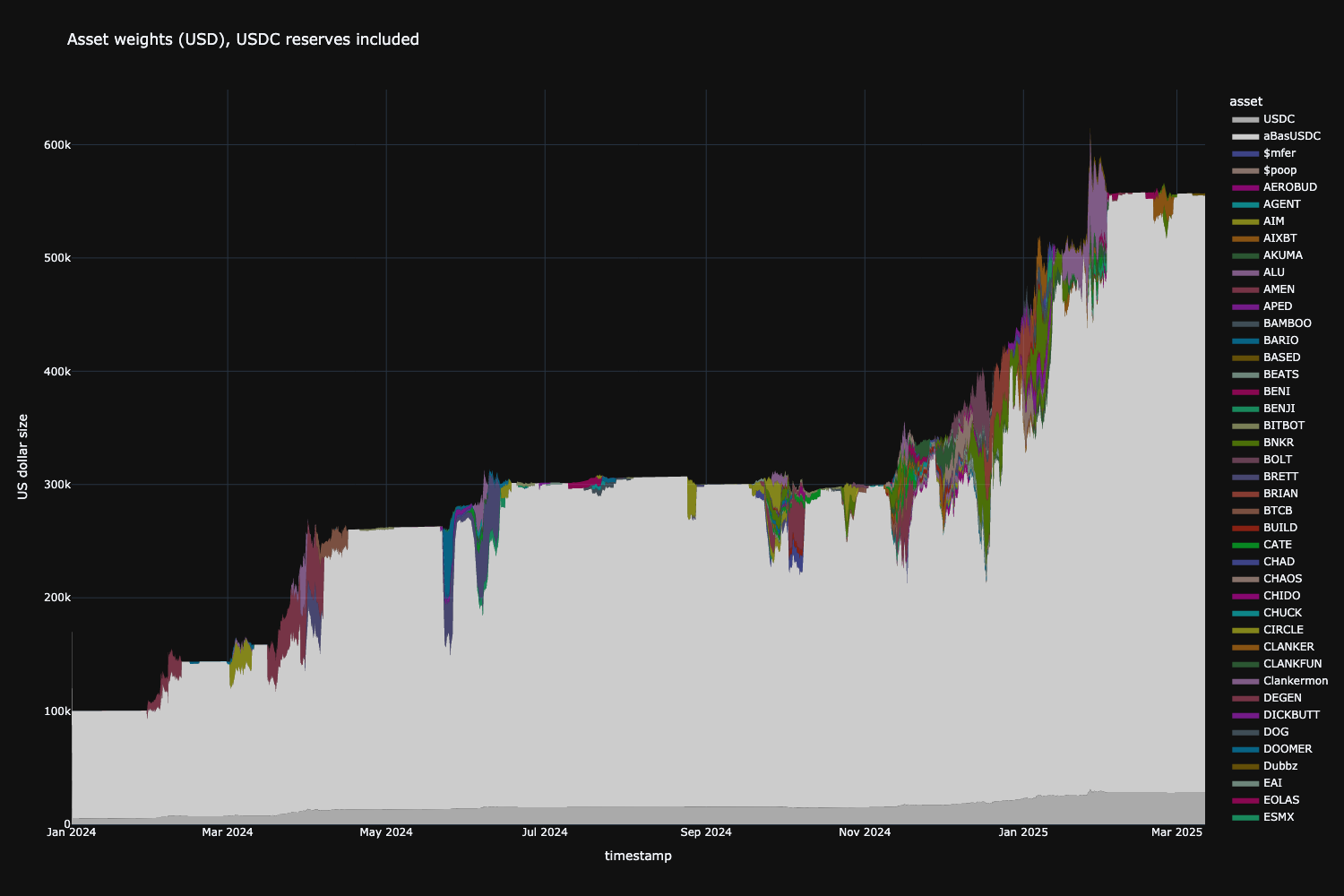

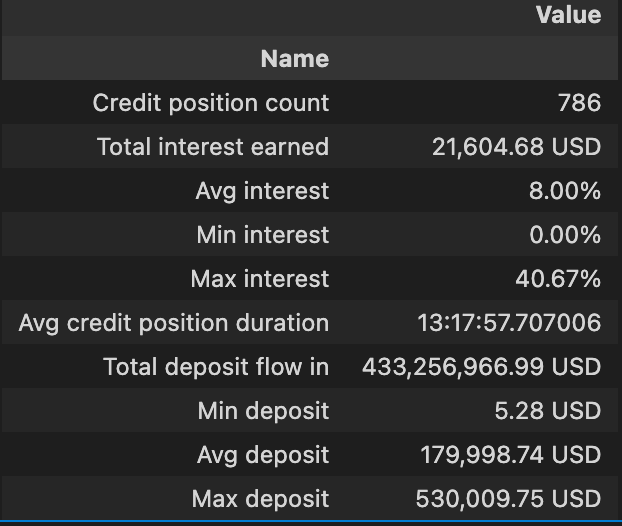

Here is the same strategy backtest, utilising idle cash by depositing it to Aave on Base. We earn variable interest of 3% - 7% on the cash.

By breaking down the equity curve by held assets, cash and Aave aUSDC interest accruing token, we can see:

- The strategy utilises cash conservatively, mostly due to position risk sizing.

- There is a lot of extra yield we can earn on unused cash.

When mixing yield elements, the strategy resembles the DeFi version of the classical equity/bond portfolio trading, where rebalancing happens between risky assets (equity) and safe yield-bearing trades (bonds, carry trade).

Even if the cryptocurrency markets meltdown to zero, the strategy should end up sitting non-idle yield-generating cash and not taking any new volatile positions.

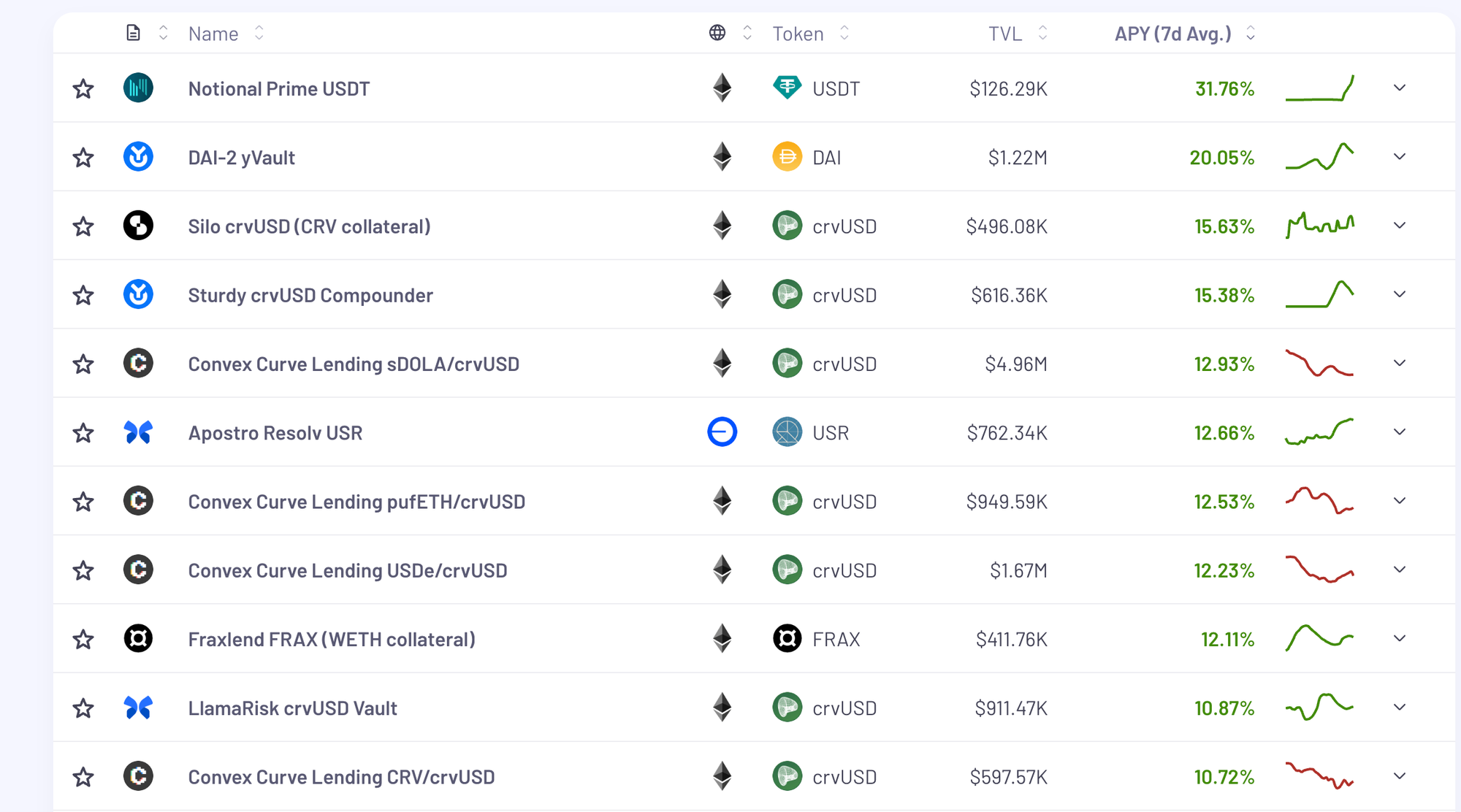

Optimising yield

Aave is the most conservative yield source in DeFi. It is easy to beat raw aUSDC interest. Here are some common options that provide delta-neutral yield:

- Lending protocol optimiser (see IPOR screenshot below) that shifts the cash between different lending protocols

- Delta neutral vault-investable strategies like Ethena, Usual, Avant

- Market-making vaults like Hyperledger HLP

The strategy can further boost its profitability and Share ratio with these options.

Trading open-ended trading universe

Trading tokens that go up-only works if we automatically consider any new tokens entering the markets. We call this an "open-ended trading universe" because when we launch the strategy, we do not know what tokens it will be trading. This is in contrast to the closed trading universe, which would only include a known set of tokens like BTC and ETH.

Trading in an open-ended onchain universe is complex, both market-wise and technology-wise. Anyone can launch a token, so thousands and millions have been launched, most of which are so-called rug pulls or low-quality efforts that never go anywhere.

The strategy applies the following filters to eliminate problematic tokens:

- TVL threshold (visible liquidity on Uniswap)

- Weekly volume threshold

- Token scam filter (using TokenSniffer)

Portfolio construction and position risk-sizing

Not all trades will be successful, and some will lose money. A key to successful trading is not to lose too much money on consecutive trades ("risk of ruin").

The strategy does tactical asset allocation to construct a portfolio. We want to keep the portfolio intact, even if individual positions are lost.

The most basic risk management concept is position sizing and diversification.

- Concentration risk: In the overall portfolio, ensure that a single asset is not too heavy compared to the rest. The strategy is set to have a maximum weight of 20% of a single asset, and if we end up with a larger one, the strategy will reduce the position. We could allow more concentration on a single asset to increase the profit, but the risk of losses in the case of issues would also increase.

- Liquidity risk: Because we are trading small-cap tokens, a lot of them have thin liquidity (market depth). Any position is constrained by the available liquidity on Uniswap v2 (AMM) or Uniswap v3 (CLMM) automated marking-making models. Or in other words, we essentially limit the position size by the asset Total Value Locked (TVL) on Uniswap.

- Rug pull risk: On permissionless and open-ended markets, most token launches are low-quality or automatically generated scams. The strategy uses a third-party automated smart contract verification service to avoid trading tokens with low-risk scores.

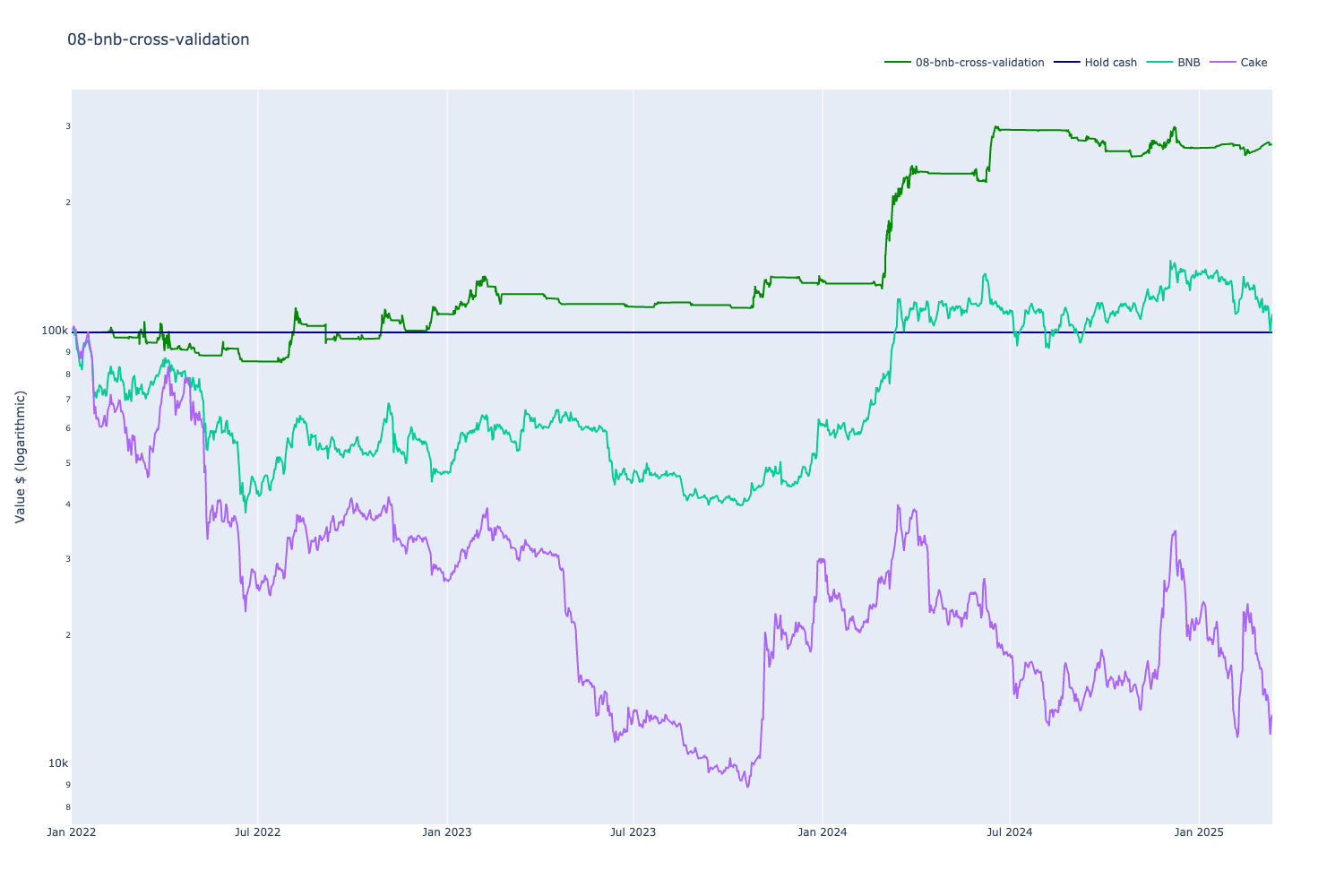

Overfitting and sensitivity analysis

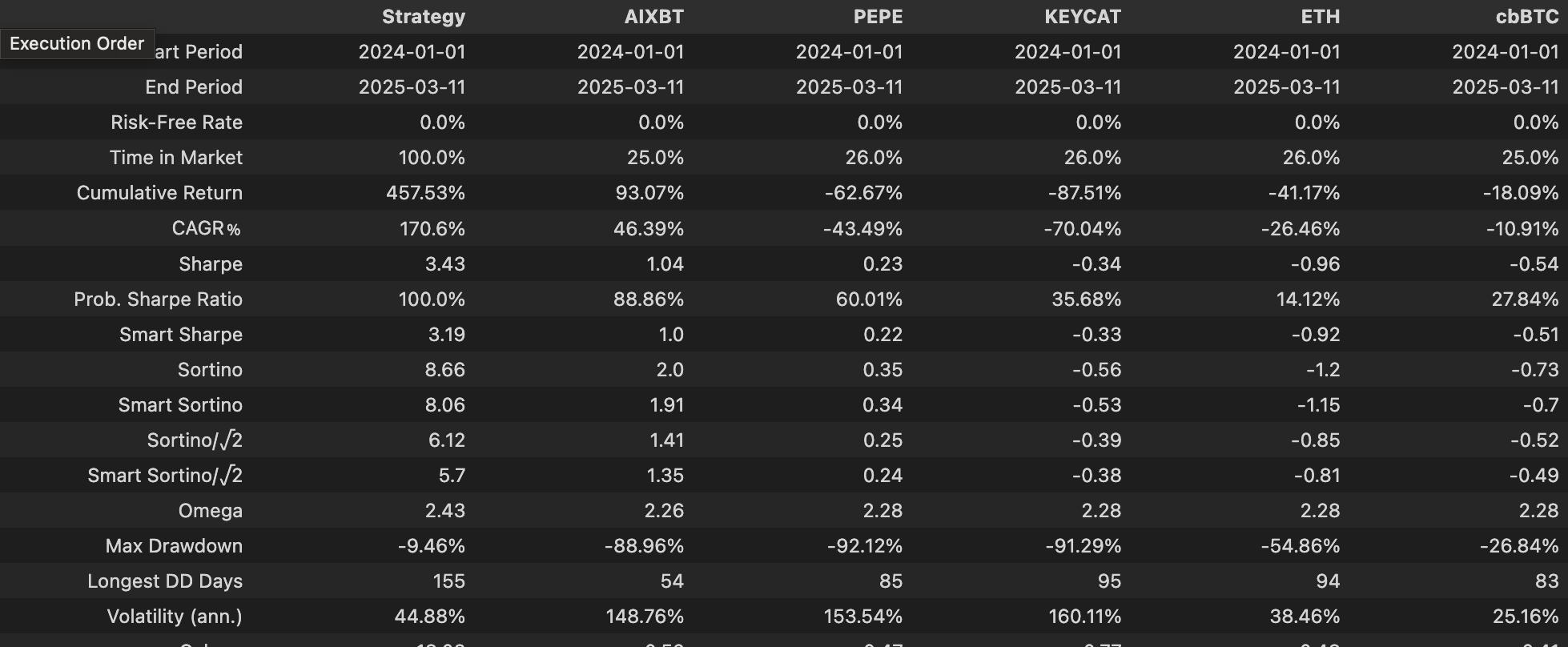

The period of 2024-2025 was particularly profitable in cryptocurrency trading. There is a risk of overfitting your trading strategy to match the data, and when the future comes and the market microstructure changes, the strategy takes losses.

We chose the Base L2 blockchain because we believe it will be one of the best EVM blockchains for trading in the future. However, Base was launched in late 2024 and has a very limited history of trading data available. Because the strategy has seen only highly profitable trading universe where "buy everything" would have been a good strategy, the strategy backtest could be biased.

To ensure the strategy is not overfitting and our trading idea is not nonsense, we also test the same strategy across slightly different markets, with different time periods, and with exactly the same parameters. While the results are not as good, the strategy still 1) makes profit 2) outperforms some of the benchmark assets on these comparison markets.

Here are some selected backtests to examine overfit and strategy validation. Because of different market profiles, like the amount of tokens and volume on the market, we need to tweak the TVL and volume inclusion criteria for every market by hand.

Future steps

This is the first iteration of an open-ended portfolio strategy that combines technical indicator-based trading and DeFi yield farming. There are many low-hanging fruit opportunities to increase both the profitability and risk-adjusted returns of these strategies.

- Improve the strategy entries and exits: By making smarter trades, we take fewer unprofitable positions, especially during sideways and bear markets. The strategy currently uses static parameters, but any kind of continuous learning process or adaptivity with machine learning and AI will likely greatly increase its performance.

- Improve interest on cash: By replacing Aave credit supply as the only source of the yield, we can get a much higher yield on the strategy treasury that is not allocated to volatile positions, as discussed in the Optimising yield section.

- Trade markets in both directions with leverage: Currently, the strategy executes only spot-market trades. However, it can increase its profit by using either Aave lending pools or perpetual DEXes for leverage. Both options also allow taking short positions on the assets, trading the market both ways.

Next steps

Please try the strategy vault yourself. You need:

- A self-custodial Ethereum wallet

- USDC stablecoin loaded in the wallet on Base

- ETH loaded in the wallet on Base for gas fees

If you have any questions, please contact us on Discord.