Decentralised exchanges and other finance protocols reached their all-time high volume on Saturday. The volume peak was due to the USDC stablecoin de-pegging its US Dollar exchange rate. While the rate recovered fast, this weekend's events may have long-term implications for decentralised finance and the banking system itself.

The run on Silicon Valley Bank and the resulting stablecoin crisis

Silicon Valley Bank, one of the banks used by Circle, the issuer of the USDC stablecoin, entered recovery in California. As of Thursday night, Circle had $3.3B or 8.7% of their reserves stuck in the bank. If Circle loses access to this money, USDC will become fractionally backed.

USDC/USD price dipped to 87 cents per dollar until recovering back near peg soon. Circle issued a statement that they may get most of their money out on Monday, and redemptions will resume normally.

Whether or how much of the stuck capital Circle can recover will become apparent next week. In the worst case, Circle holders may expect an 8.7% haircut. In the best case, nothing happens. We may also expect further bank runs, in the US and elsewhere, in the short term.

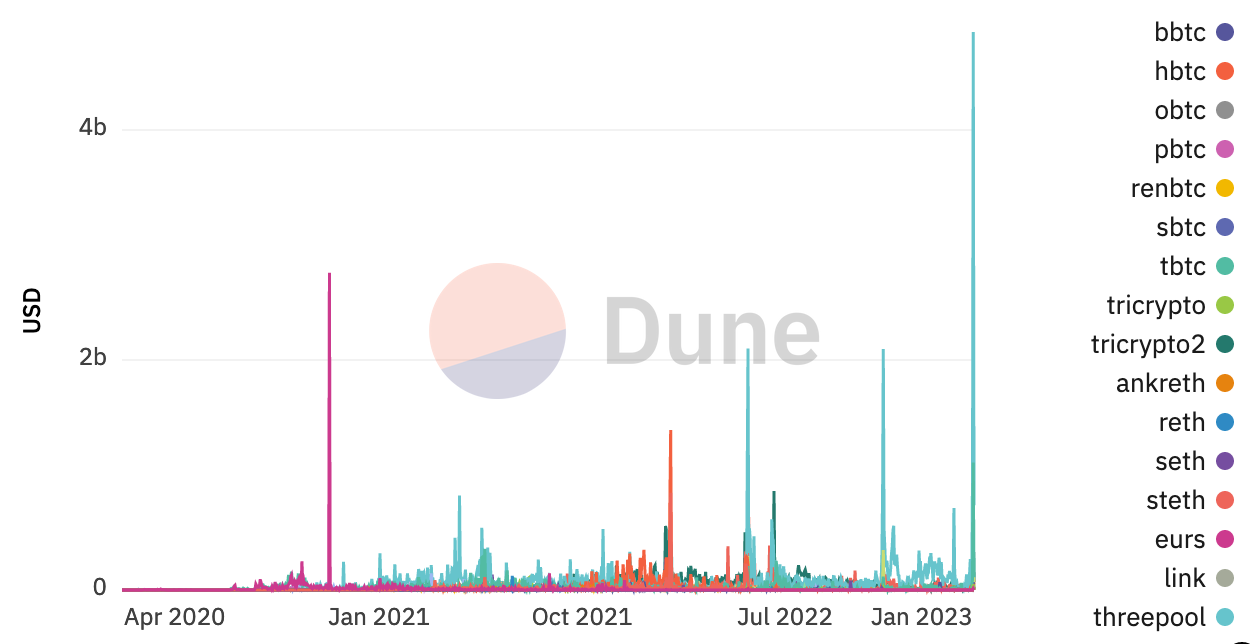

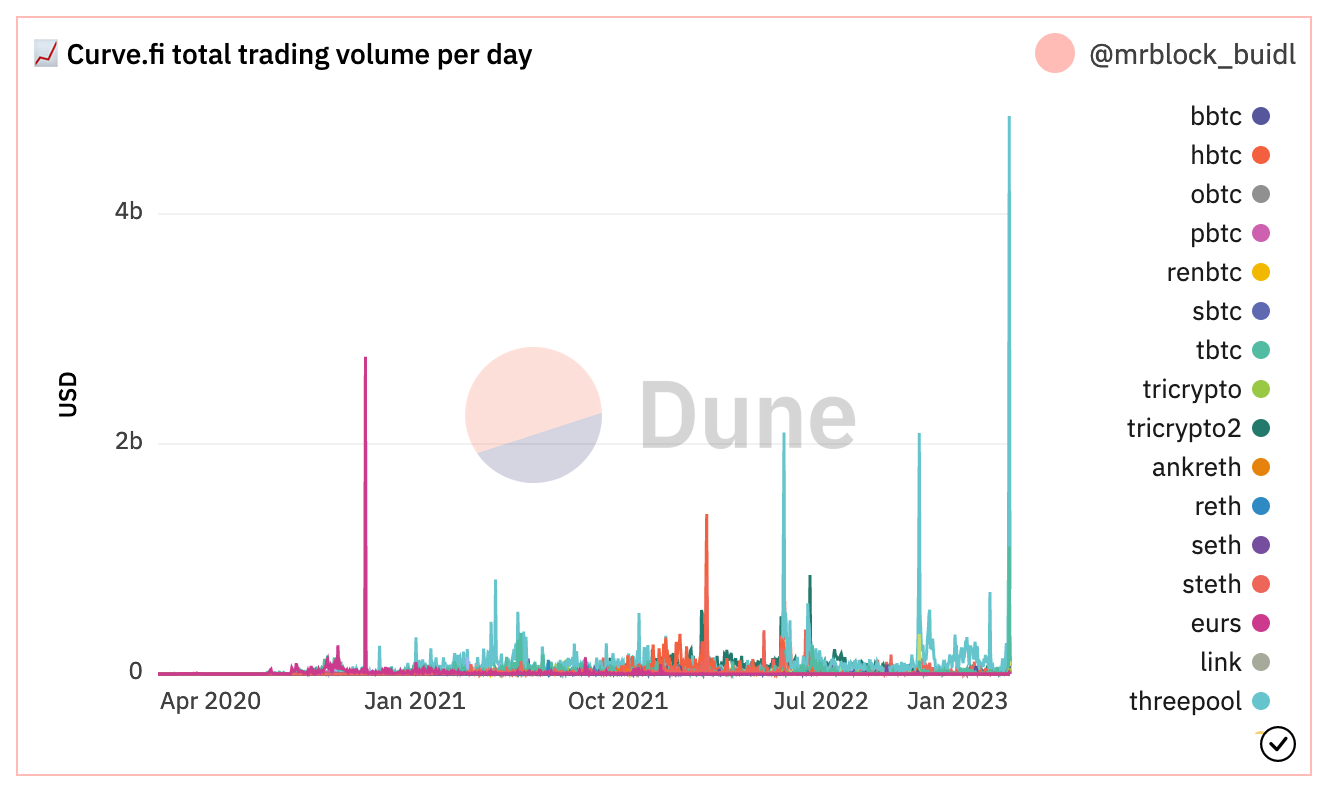

The all-time volume high on DEXes reached

The de-peg of the USDC/USD exchange caused multiple effects that spurred furious trading. The peak daily volume was roughly two times the previous peak.

There was rampant speculation on whether USDC will recover, and you could trade against this by longing USDC in USDC/USDT (Tether) trade.

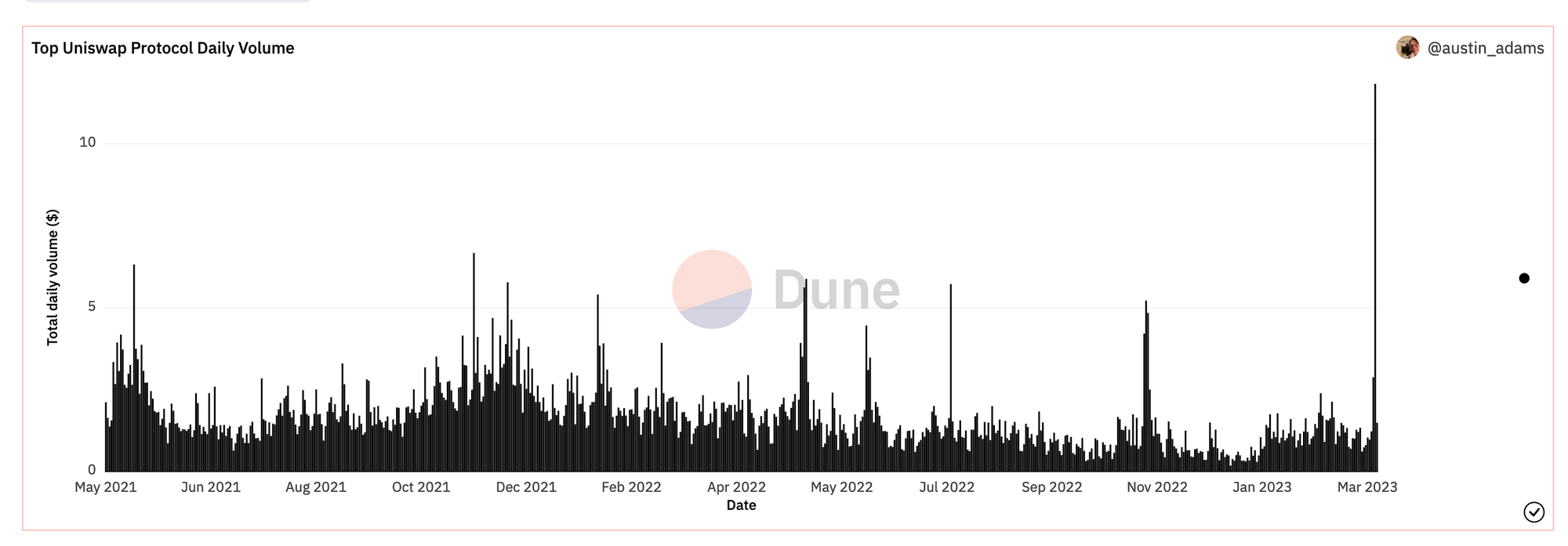

Uniswap v3 reached an all-time high volume.

Curve, the original stablecoin to stablecoin DEX, reached an all-time high volume as people were swapping between USDC and USDT and speculating whether the peg will recover.

Aave USDT reserve pool utilisation reached 100%, as all USDT was loaned out for long USDC leveraged trade.

Huge spike in withdrawal volume of $USDC from $AAVE also a large spike in borrowing volume of $USDT. Market is preferring one stablecoin over the other. The advantage for AAVE & #DeFi is the interest rate changes in real-time to compensate. $eth $link pic.twitter.com/FYes3atrkM

— CanuckLink.eth 🍁⬡ (@CanuckLink) March 11, 2023

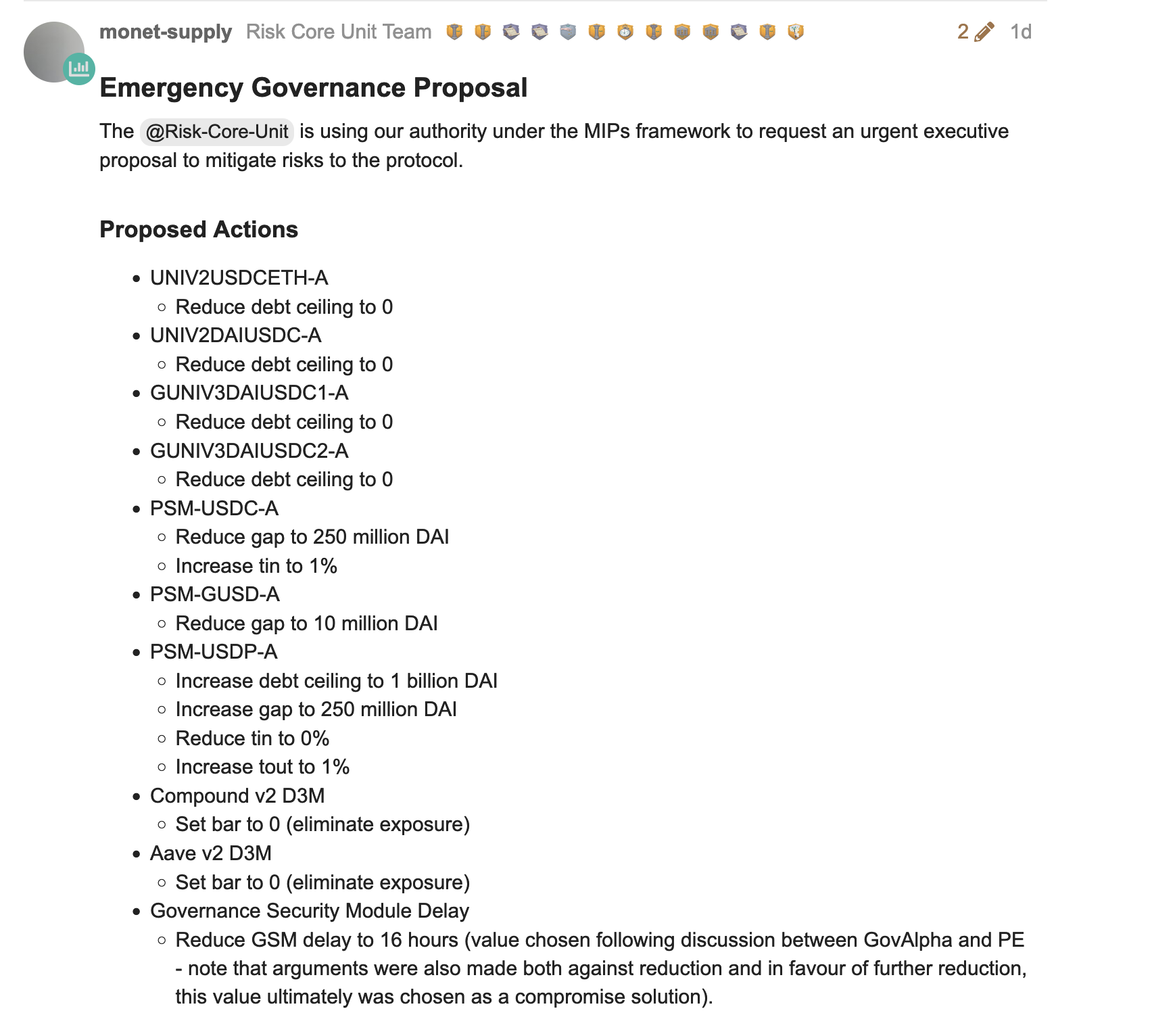

Some DeFi services like MakerDAO had hardcoded USD value to 1.0 US dollars per USDC which was no longer true. MakerDAO had to engage in emergency governance voting to mitigate the risks.

On many DeFi perpetual swap marketplaces, the interest rate for short/long positions reached 100%.

All these led to an all-time high volume peak in decentralised markets. This demonstrates that DeFi markets can handle increasing amounts of volume, and work 24/7 when the traditional banking system IT breaks.

The future implications of the USDC depeg for DeFi

The event was a hard hit on the reputation of the USDC stablecoin, as it has enjoyed the status of one of the most trusted stablecoins due to its transparency. This is different from the main competitor USDT, which opaque structure has been a suspect of bad investments for the best part of the last decade.

The remaining 23% ($9.7bn) is in cash. Last week, we took action to reduce bank risk and deposited $5.4bn with BNY Mellon, one of the largest and most stable financial institutions in the world, known for the strength of their balance sheet and as a custodian.

— Jeremy Allaire (@jerallaire) March 11, 2023

$3.3bn of USDC’s… https://t.co/Bm1rZaTEPK

However, the weaknesses of the US banking system become apparent to everyone in this episode: it feels like not much has changed since the Great Financial Crisis of 2008.

- There might still be US banks that are overexposed to rising interest rates.

- There are rumours about a backstop fund to save any potentially failing US banks.

This all will reflect decentralised finance:

- USD is the world currency trade, especially decentralised finance. The second runner-up, EUR is well below 1%.

- Purely crypto asset-backed stablecoins like RAI and LUSD might see a blip in popularity now, as they are deemed to be outside the banking risk.

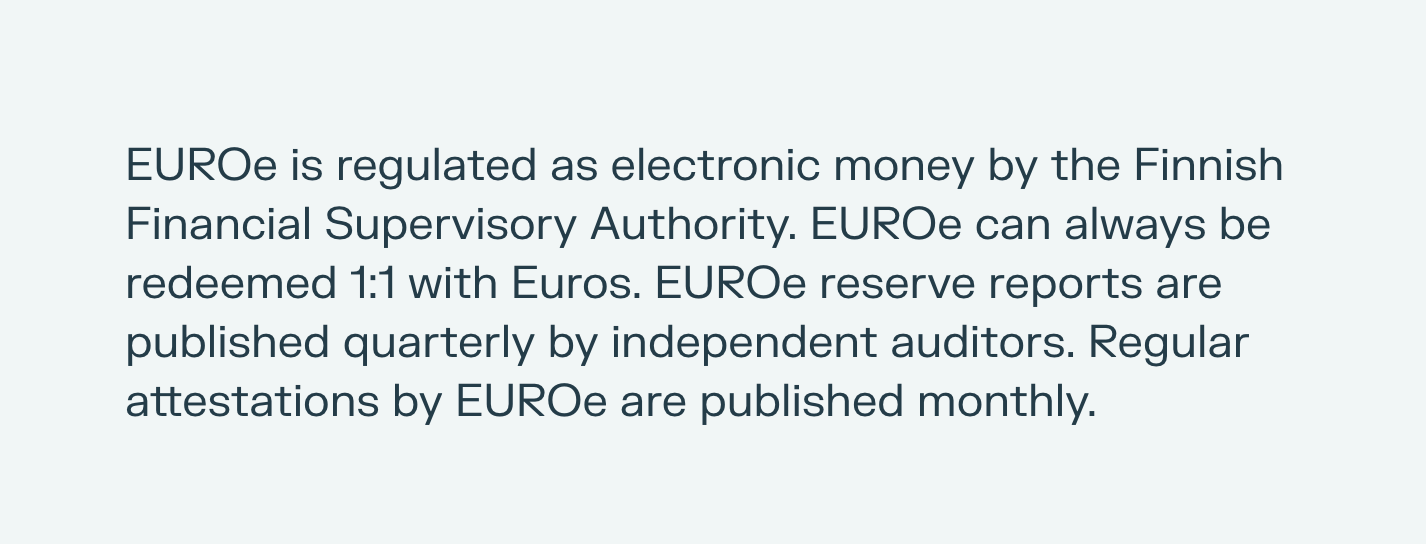

- New fiat-backed stablecoins, with stricter regulation and better transparency, like EUROe may start gaining popularity.

- Paxos USDP, a 100% US Treasury Note-backed stablecoin, may see an increase in popularity despite Paxos's recent fumbling with BUSD. 100% treasury note reserve is not exposed to counterparty risk with banks.

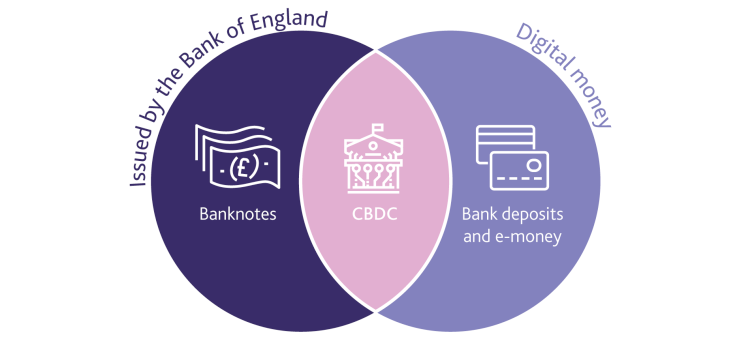

Shall we see the end of banks and the rise of CBDC?

The events like this will make people ultimately question what money is and the risks of having money in your bank account. The multitier banking system in all countries today is because access to safe central bank money is limited to banks only; consumers cannot directly hold safe central bank deposits. The alternative system is CDBC or Central Bank Digital Currency, where everyone can access central bank money.

It is impossible to create a so-called narrow bank in the US that would only hold your money safely and not engage in any loan business. This is because Fed wants to banks to participate the money creation: if people were given a choice to keep their money safely outside banks, no one would longer make bank deposits, and banks would become unnecessary.

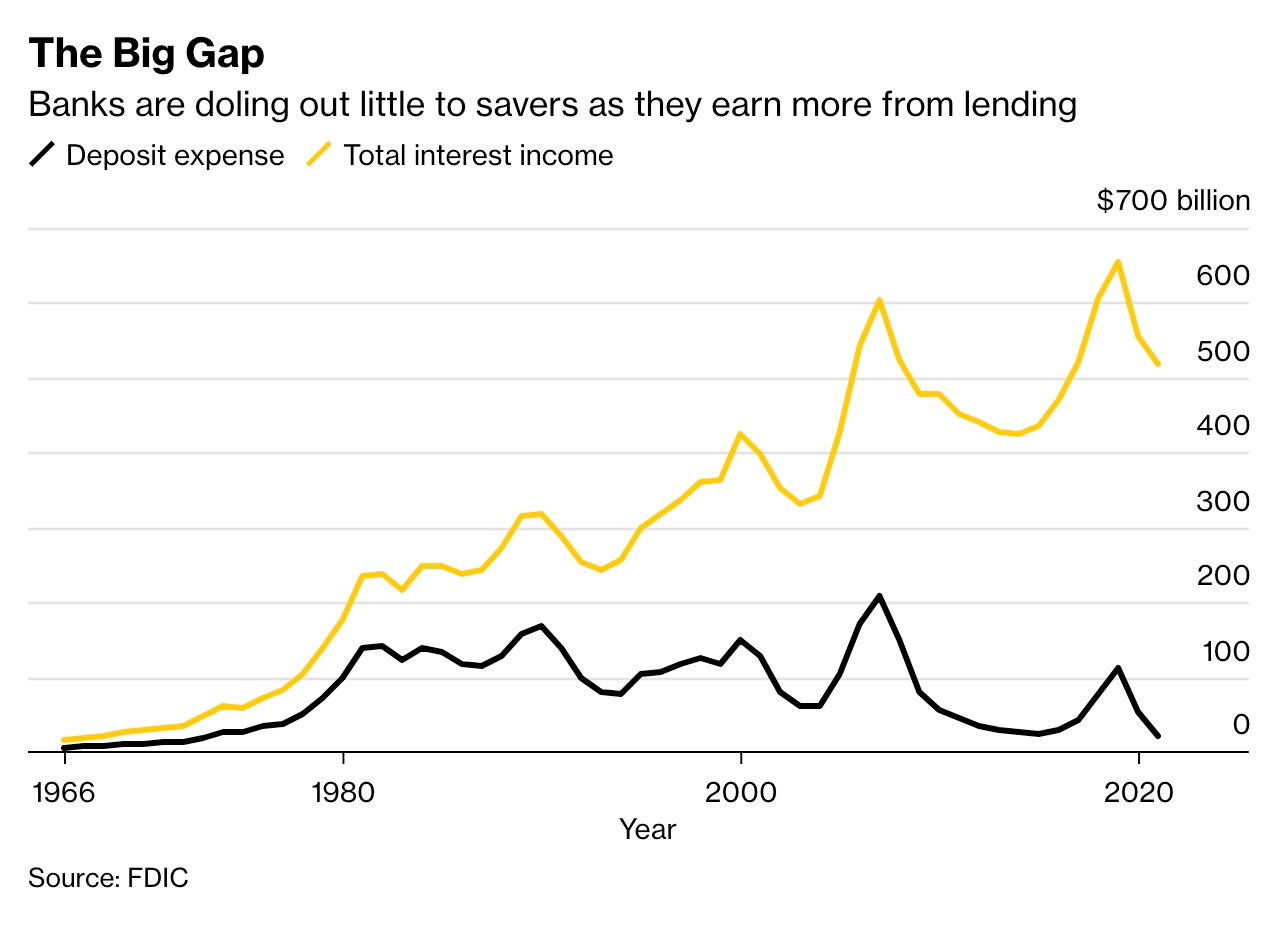

It is not a rational risk to give your money banks the meagre interest payments you can receive today. We can see that the interest banks pay on depositors has steadily fallen, and the bank's share from the interest themselves has increased. This is even though automation has massively made banks more efficient since the 80s.

While it is unclear whether the future of money is Bitcoin, Defi or CBDCs everyone agrees it is not the current banking system.