Blockchain technology delivers innovation. The essence of this innovation is often lost in public discussion - arguments focus on the negative perception of blockchains. We examine where and why blockchains are presenting unbeatable competition to traditional financial services.

As an example, we present Uniswap's decentralised exchange and compare it to traditional exchanges, both crypto and stock. Due to the increased efficiencies in the new smart contract business model, Uniswap can deliver a 20x lower cost to a consumer than one of its traditional competitors. Uniswap's open and transparent nature also ensures markets are fairer, with less room for detrimental business practices.

Background

Lately, there have been discussions of blockchain not solving any real problems. Recently David S. H. Rosenthal, a well-known computer scientist gave a talk where he criticised blockchains and explained why he does not believe they create value. This was picked up by many technology influencers, like Mark Russinovich, the CTO Microsoft Azure. While some of the criticism presented is valid, the criticism focuses on the weak areas of blockchain technology and only builds upon the history of cryptocurrencies. These smart people are experts in their own sectors, but might not study the latest engineering deliverables or the status of contemporary cryptographic, consensus and fintech solutions.

We look beyond the often-repeated arguments that might have been true some years ago, but are debunked today:

- Energy consumption: only one of the top #20 tokens by market cap uses energy sensitive proof-of-work consensus (Ethereum Merge will transition the chain to proof-of-stake in summer 2022).

- Terrorist and criminal usage: based on facts and data this is a politically exaggerated issue, as seen in 2022 State of Crypto Crime and National Money Laundering Risk Assessment 2022.

- Speculative risks with cryptocurrency investing: not different comparable to NASDAQ stock volatility where tech stocks are down 75% from all-time high and in any case stablecoins are taking over as the medium of transfer-of-value.

These arguments do not consider use cases where blockchains create value for their users. Outright dismissing blockchain technology is not rational. Fundamental value is created and this value creation is hard to replicate in traditional business models. We already see what kind of measurable tangible benefits blockchains provide to their users today.

Market operational efficiency

A market is reported to be operationally efficient when participants can execute transactions and receive services at a price that equates fairly to the actual costs required to provide them. When transaction costs diminish, an economy becomes more efficient, and more capital and labour are freed to produce wealth.

Transaction costs, or from here on just generally fees, are unrelated to the asset itself you need to pay for to make a trade. This principle can be applied to both the liquid markets (stock, cryptocurrency) as well as illiquid, non-fungible markets (real estate, NFTs).

Fees can be defined as

- Spread - the price difference between the best ask and bid offer

- Fees to the market makers (often related to the above)

- Fees to the exchange operators ("commission")

- Fees to the infrastructure providers

- Other fees and non-transactional costs, like withdrawal fees and account opening costs

Beyond the fees, we have a price impact which is a result of available liquidity. The more liquidity, the lesser the price impact will be. Price impact is independent of fees - it is more a result of the size of the market than the operational efficiency itself.

The fees on liquid markets are usually measured as basis points (BPS). A basis point is a per cent of a per cent. While there can be a fixed price per order, often the transaction price on a liquid market is just its BPS fee. For example, a 3 BPS fee on a 500 GBP trade translates to 500 * 0.0003 = 0.15 GBP, or 15 pence, cost.

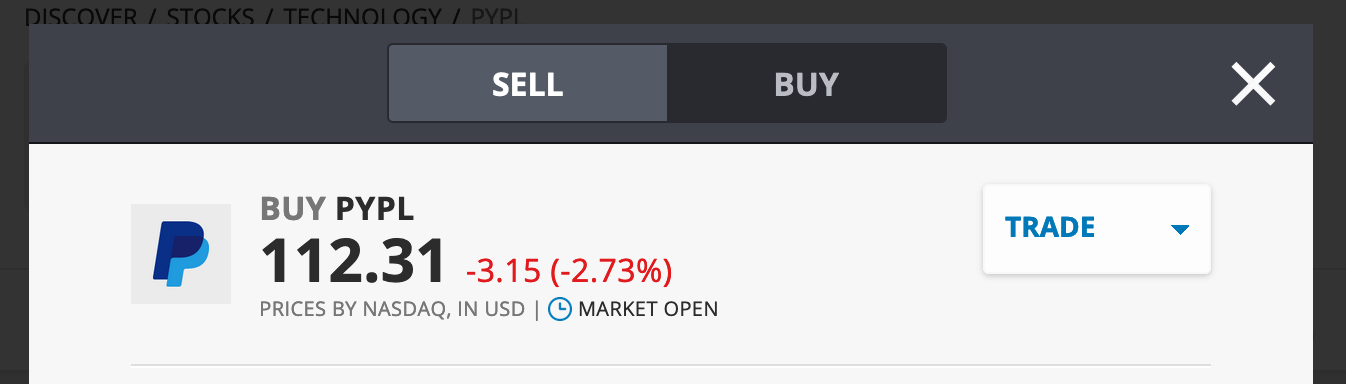

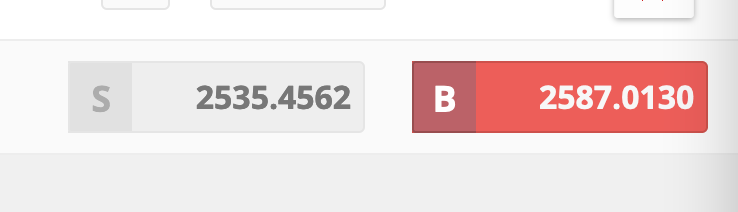

Here are two screenshots from an online stock broker for PayPal (PYPL) stock. You can see the broker gives you a different price for buying and selling. The difference is the spread. The spread for PYPL is 1 - (112.20/ 112.31) * 10,000 = ~9.8 BPS. Even though trading is "0% commission" the user ends up paying for the participation in the form of spread losses. If you are buying or selling you are paying ~5 BPS over the theoretical mid-price.

Meet Uniswap: the world's most efficient market

Uniswap v3 is the third version of the well-known automated market maker, now with concentrated (ranged) liquidity provision. Uniswap is available on Ethereum Virtual Machine (EVM) based public blockchains, including Ethereum mainnet, Arbitrum and Polygon.

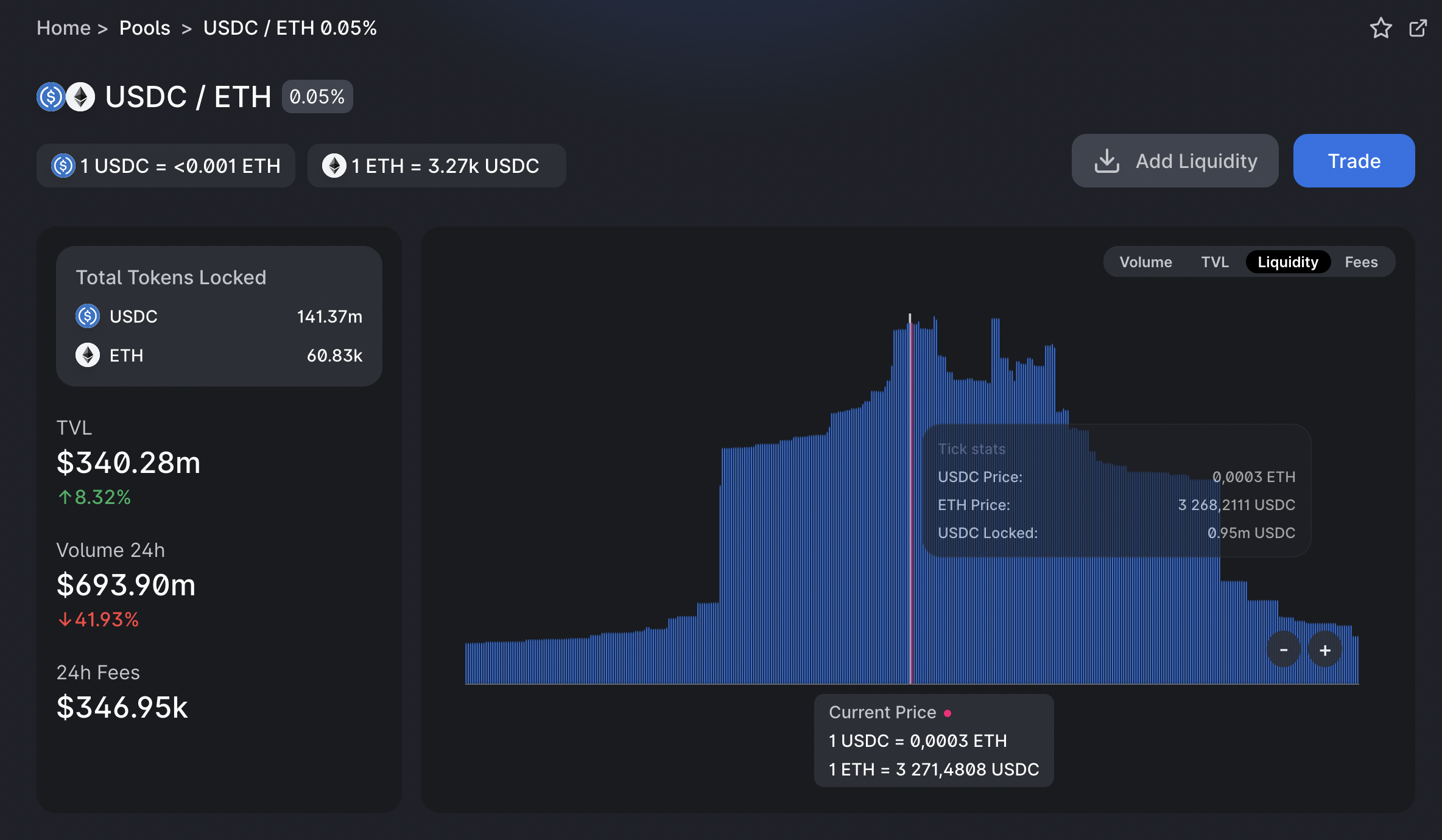

Unlike discrete, order book based bidding, Uniswap introduced the concept of ranged liquidity, also known as concentrated liquidity. In a ranged liquidity model, a liquidity provider (market maker equivalent) offers assets on both the ask and bid side. Here is a range diagram for ETH-USDC 5 bps market:

In the ranged liquidity model, trades, or "swaps" as they are called, have zero spread. Any fees for the trade go directly to the liquidity providers. Although taking a commission for the exchange itself is possible, Uniswap is not doing this yet. Uniswap's closest competitor, Sushiswap, is charging 16% on liquidity provider markup for its token stakers.

Originally Uniswap v3 supported 5, 30 and 100 bps fee markets. After the launch, the activist investors Alex Kroeger and Getty Hill made a proposal for 1 bps markets, as a successful demonstration of decentralised protocol governance by use of tokens. At the moment 1 bps markets are available only for non-volatile assets, like stablecoin pairs, comparable to the traditional finance FX markets. Nonetheless, their mere existence is showing there is a cost race to the bottom in progress.

The comparison methodology

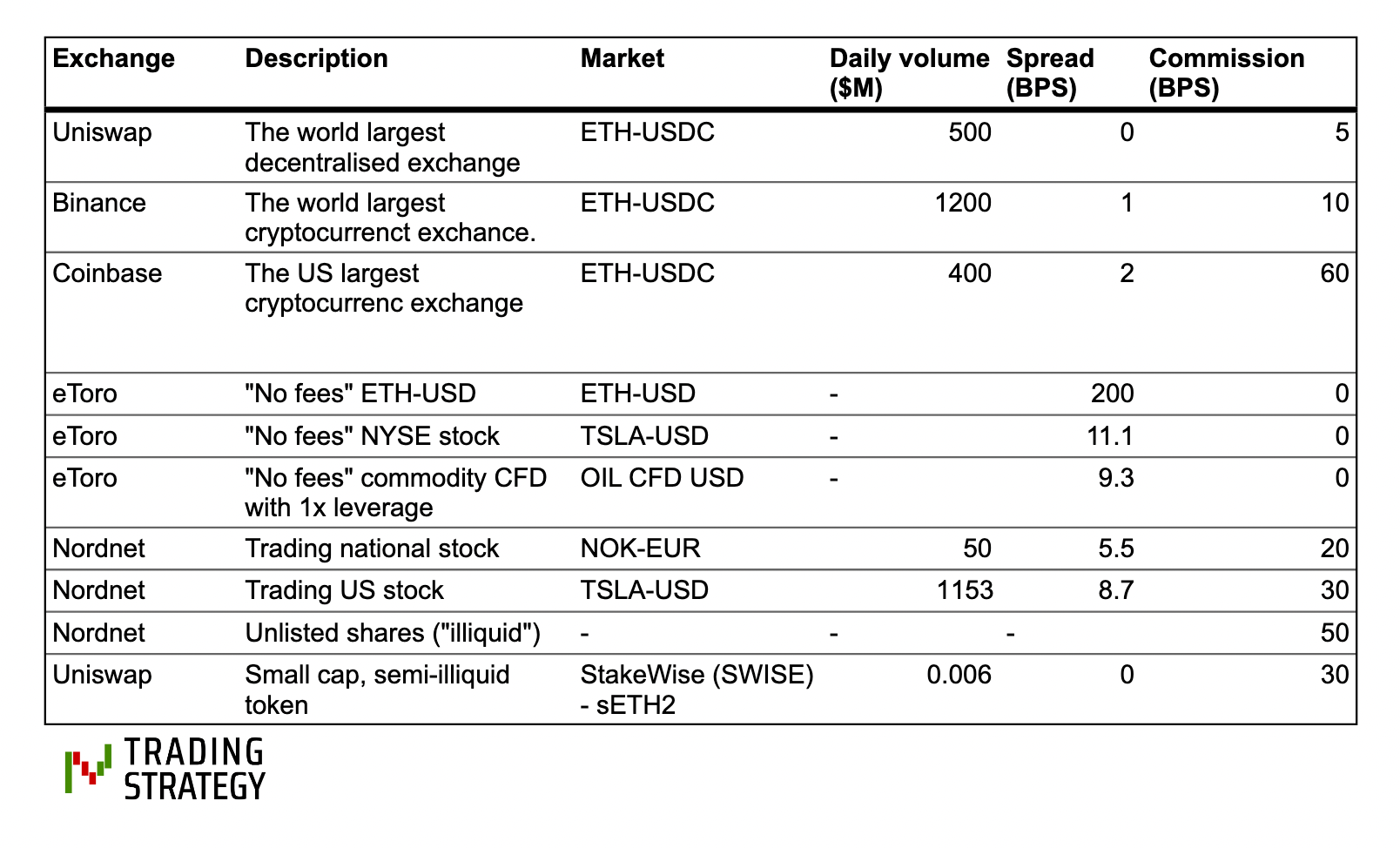

To demonstrate the market operational efficiency of Uniswap, we compare it to the state-of-the-art exchanges and brokers. This is by no means a scientific study; We compare prices of a single day to drive our point home.

We compare Uniswap's ETH-USDC market to the world-leading centralised cryptocurrency exchanges Binance and Coinbase. We also compare to a "no fees" online broker eToro on the NYSE stock market, CFDs. We also compare to a traditional small broker Nordnet and its brokering of publicly listed stock on Nasdaq Helsinki, a small national stock exchange.

No discounts given or taken

The comparison is done from the point of the "retail" trader - assuming low price impact-free traded amount, like $1000. We ignore all discounts, kickbacks and such available for large traders or traders with a direct seat in a stock exchange. We also account for withdrawal fees. We also assume the market order (taker order) type, as this is the typical trade that retail investors make.

Stock market comparison

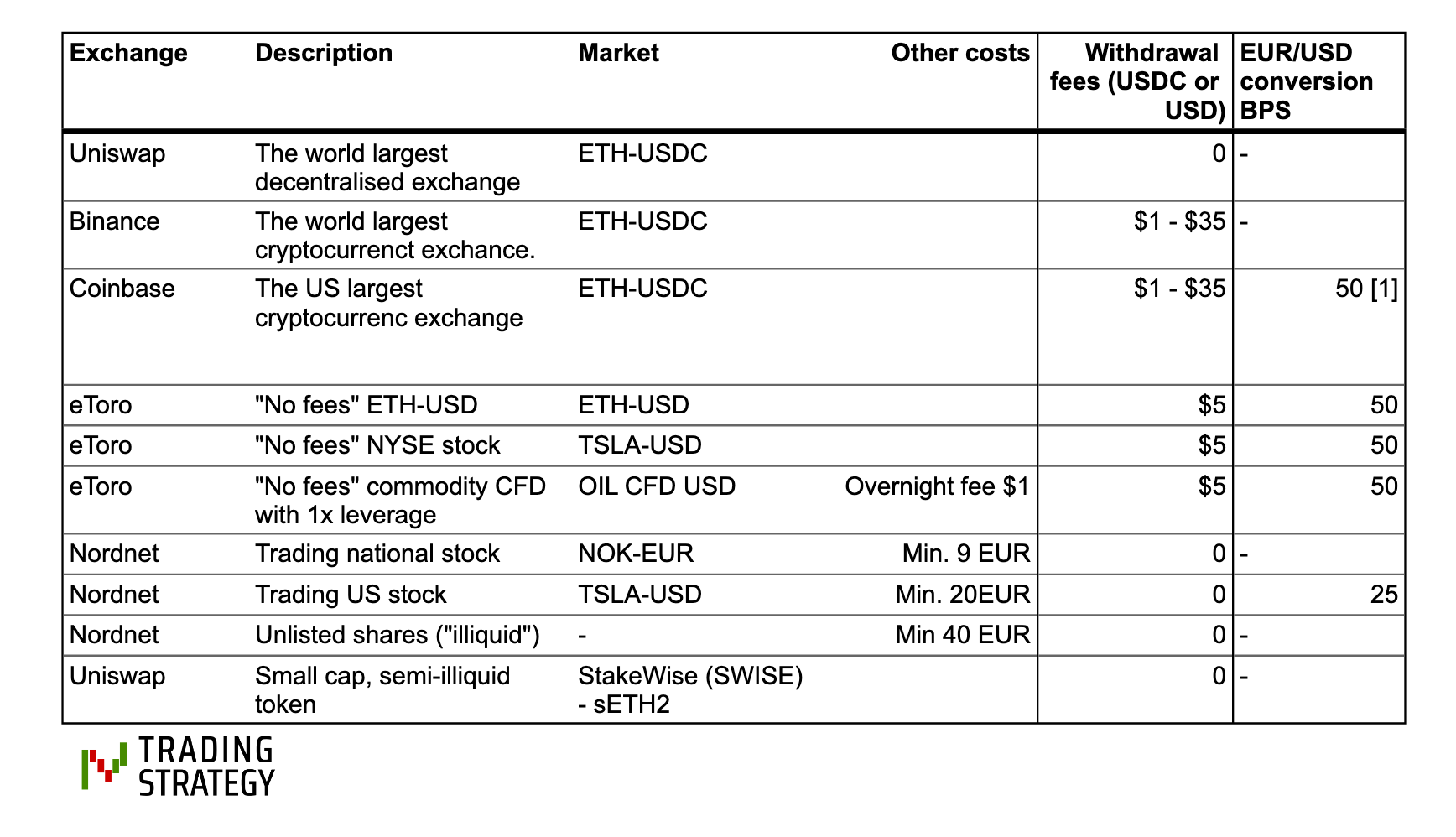

Nordnet and eToro spread measurements were done by taking the best ask and bid samples from the respective web user interfaces at 16:33 local time. We also included EUR/USD conversion fee the online brokers take on deposits and withdrawals. The equivalent fee in the cryptocurrency markets would be EUR/USDC trade cost on any order book.

For further comparison, we included Nordnet's "unlisted shares" price and then take a random small market cap token from the Uniswap list, to better understand AMM pricing for low liquidity assets. However, for low liquidity assets, the price impact is the dominant factor and compared to this trading fees are insignificant.

Here is a screenshot of Coingecko ETH-USDC market page, taken 11.3.2022 that we use as one source for our data.

We also measured the spread on eToro's ETH-USD pair. eToro (Europe) Ltd is an EU financial services company authorised and regulated by the Cyprus Securities Exchange Commission (CySEC). eToro is not a cryptocurrency exchange but still offers crypto brokerage. eToro's spread was 200 BPS or 2%. On this EU regulated "no fees" broker you end up paying 20x fees you would pay on a decentralised exchange and ~4x more than Coinbase, the US competitor.

Blockchain transaction costs

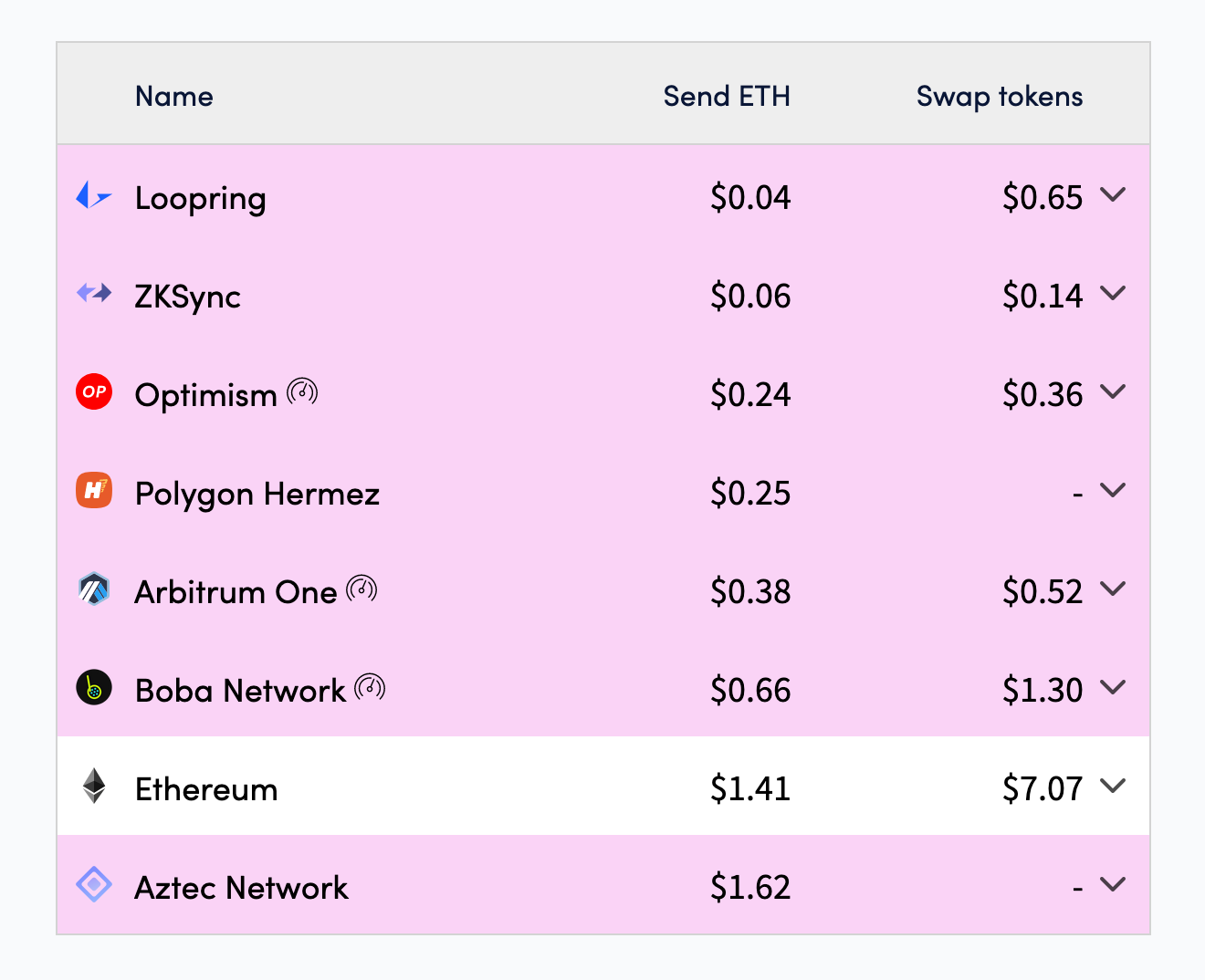

For blockchain transactions, costs are paid to the block producers (known as "gas fees" in Ethereum parley). As there was no good service to compare transaction costs across blockchains in general, we took the lowest swap fee taken from l2fees.info. Note that this does not reflect the current Ethereum mainnet proof-of-work transaction fee, but presents the best easy to verify the on-chain cost. The popular layer 1 chains like Avalanche and Polygon are in-line with the ZKSync gas fee. Non-EVM blockchains like Solana may push this cost 10x further down.

Fee sources

The following sources were used to assemble the fee information for the comparison:

- Coingecko ETH-USDC

- Coinbase Pro fees

- Binance fees

- Etoro fees

- Nordnet fees (the page in Finnish, also available in Swedish)

- Nordnet spreads

- l2fees.info

The comparison result

Assuming free USDC/USD fiat on/off ramp through Circle or Coinbase, Uniswap is the most cost-efficient ETH-USD market for a retail trader.

With ~5 BPS trade costs Uniswap ETH-USDC beats the best cryptocurrency exchanges and also is in line with online stock brokers. From the Coingecko screenshots above, we see Uniswap volume is the 2nd highest and 50% of the highest comparable pair Binance ETH/USDT. Thus, it is quite fair to say the markets are already realising the efficiencies of decentralised markets.

The Uniswap 5 BPS total fees are comparable to eToro "no-cost" liquid stock 10 BPS spread trades. Uniswap does not have withdrawal and deposit fees, so its total trading cost might be lower already today.

We also added some other costs as these are not immediately visible in spreads or trade commissions.

Efficiency factors beyond transaction costs

Furthermore, because Uniswap runs on a public blockchain, there are efficiencies centralised markets cannot match

- No counterparty risk.

- No withdrawal or deposit fees.

- Direct-to-investor or no broker fees.

- Markets operate 24/7.

- Due to the usage of a public blockchain, data is freely available for everyone at the same time, making the markets fairer. There is no hidden cost of delayed market data.

- The software that runs the exchange is open source and can be audited by anyone for mistakes in fee structure and such. Less regulatory intervention is needed as the market participants can self-audit their venues.

- No vendor lock-in. You can take your tokens to any other exchange if you are not happy with the service for almost zero fees and no hassle.

- The listing process is automated. For the asset issuer, listing costs are basically zero, both cost and time-wise.

- Less staff needed: because the activity is governed by smart contracts, there is less need for front office, middle office or back office staff (finance)

Why do public blockchains solve trading problems more efficiently?

Uniswap is a favourable example of a blockchain technology that improves upon centralised, proprietary solutions. It is important to ask the question "why is this?".

The opponents of blockchain technology often argue that anything implemented on a blockchain can be more efficiently implemented on a private server, like on the Microsoft Azure cloud. Maybe - if you only count the cost of electricity of a server fleet. In practice, power cost is not a significant cost for any software-as-a-service business and business costs are created elsewhere.

We argue that blockchain technologies have inherent advantages that cannot be matched by proprietary solutions and business models in long term.

Creating efficiency through openness and transparency

Public blockchains rely on three cornerstones

- Open source: Blockchains and decentralised finance protocols are open-source

- Open data: Data is free to access and available for everyone

- Open network: No barriers to entry to make a transaction

We examine how these ideas have been historically powerful alone, and then conclude why combining them will create novel benefits.

Benefits of open-source

The open-source software movement started in the 80s as a branch of the free software movement. The key promise of open-source is that software can be created more cost-efficiently because of cooperation and reusability. Compared to proprietary software development, the open-source promise touts no vendor lock-in costs, a larger talent pool, better career paths, better developer motivation, easier adoption with less license hassle, guaranteed software continuity and so on.

The sweet spot of open source, and its more generic cousin open innovation, is when small or medium-sized enterprises can innovate and collaborate together and thus compete against large enterprises. This is especially interesting in sectors dominated by large oligopolistic companies.

The most well-known success story of open-source is the Linux kernel. What started as a hacker movement in 1991 and evolved into a mainstream server-side operating system in the early 00s. It was an uphill battle: the large established companies like Microsoft downplayed, FUDed and muddied waters around Linux. It might have bought some time, but in the end, was in vain. First Linux put all commercial UNIXes (HP, Sun, IBM AIX) out of business. Finally, Linux put Microsoft out of misery in the mobile phone OS market. Mobile phone vendors trusted open Android over Windows Phone, because they had more control over the ecosystem. Ultimately Microsoft did a $7B write-off on its mobile phone business, quite a victory for "communist thieves".

Linux, serving as the foundation for the software business, led to the creation of Google, Android and Tesla. Today, Linux powers billions of devices. But more importantly, Linux is the core component of hundreds of thousands of products and businesses. Because of its open-source nature, these companies can innovate and build together in ways they otherwise could not.

Benefits of open data

While data has existed since the time of writing, data accessibility enabled by the Internet has increased the impact of open data by orders of magnitude.

A data commons is an interoperable software and hardware platform that aggregates (or collocates) data, data infrastructure, and data-producing and -managing applications in order to better allow a community of users to manage, analyze, and share their data with others over both short- and long-term timeline (Wikipedia).

Open data drives innovation. Also, as we earlier discussed, proprietary data drives market inefficiencies and profits of oligopolies.

Blockchain, the use of pseudonymous addresses and public-key cryptography, take this to another level with its innovation of separating real-world identities from ownership and authorization. Without this separation, data could be a liability and subject to complex or impossible licensing arrangements. Because there is no such liability, parties can transact with each other more easily, as they do not need to worry about what happens with their private information.

Benefits of open network

In the early 90s, hypertext transfer protocol (HTTP) started the Internet "information highway" boom, which later led to the creation of e.g. eCommerce, online banking, social media, and remote working industries. The main driver of Internet adoption was its open nature - anyone was free to set up their own web server, home page, or an online store, no permissions asked. Although some of the same original ingredients existed already in the 90s permissioned networks like Microsoft Network, the Internet quickly took over. Public blockchains take the Internet's permissionless model to financial services, making the barrier to entry very low cost.

To transact with a public blockchain, you pay a fee in the form of a transaction cost that roughly equals the actual cost of the transaction to be included in the ledger, or computational units consumed, by the blockchain block producers. The experience is frictionless: there are no software licenses to be bought, no business negotiations to be done, no paper agreements to be emailed back and forth, no API keys generated, and no marketing spam to be accepted. This makes transactions on public blockchains the ultimate process improvement in finance.

In theory, the traditional finance systems could become open networks and match the model set by public blockchains. But in practice, they cannot. Traditional finance is built around high trust networks. This is because of

- Control: ensure that profit is made and kept in a closed circle, fear of competition

- Lack of system resilience: a malicious participant can harm the system

For example, the stock market order book's direct API access is carefully cultivated and only available for certain members of the stock exchange. Everyone else needs to access through a broker that acts as a middleman. This is due to the legacy when the orders were still settled through a hierarchical middleman network, but also because the stock exchange can make more money by keeping the gated access to certain participants.

Another example is the EU PSD2 directive. The banks have had a massive moat as they have held people's money but the only way to access this money was the way the banks told you - through their (often horrible) online portals. There was no API, you could not create an app that spends money, or makes a transaction, from a bank account. This is about control and managing competition for the banks: they are afraid someone else creates better products and reduces banks to dumb pipes.

The EU likes competition and saw the issue of banks hindering innovation with their customer stickiness moat. The EU then tried to enforce "you must provide the API access" principle through the regulation called Payment Service Directive 2 in the hope to spur some competition. But the law did not produce effective software - the implementations are brittle, faced with conflicts and challenges. The implementation itself is anything but open - TPPs (third party providers) still need to get a license to access any incompatible APIs. Or to put it bluntly: the PSD2 model is a bit of an oxymoron, you need to make a contract with a third party to get API access to your own bank account. PSD2 has not been a huge success and did not spur the fintech innovation its political promoters touted.

Who is being disintermediated?

New technologies like public blockchains are disruptive innovations. The benefits they promise are coming through disintermediation - by eliminating middlemen in the process and replacing them with software and automation. So who exactly is being replaced in the case of decentralised markets?

If we look at the exchange fees we discussed earlier we can see that exchanges are taking their commission in the form of spread and fees. These are then further divided between the exchange itself (Coinbase, Binance) and its market makers (in-house, third party), often paid in the form of kickbacks through opaque arrangements. The market maker arrangements are trust-based or volume-based - a normal layman can never get the same trading deal as one would get as a "designated market maker." Maybe the shadiest form of these deals comes from the public equity markets from a no-fees online broker Robin Hood and its Payment For Order Flow (PFOF) because of the conflict of interest of a broker making more profit when it is "saving in customer transaction fees."

In decentralised markets, such shenanigans do not exist. Anyone can be a market maker, or a liquidity provider as they are called, on Uniswap. Everyone has the same terms to access the markets. If there are special arrangements between parties they need to go through a public governance voting and they will be visible on-chain. This forces the markets to be fairer and more competitive. Furthermore, compared to the traditional finance world, direct-to-investor exchanges eliminate the need for brokers and self-custody eliminates and reduces the need for custodians.

Crypto exchanges enjoyed fat profit margins in 2021. But with the ever-increasing share of decentralised exchanges, this is changing. Naturally, market makers are salty about this development. Although Uniswap's ranged liquidity model is new and yet to be proven, data is still being gathered, it looks like market makers can stay profitable, but with thinner margins. This ultimately means that exchanges and market makers can extract less profit and this directly translates to less fees for consumers.

Issues with decentralised finance

Decentralised finance did not truly get started until the summer of 2020, or the so-called DeFi summer. Earlier, blockchain technology was too primitive. It took years for Ethereum software development tools to reach the maturity level to crank out protocols like Uniswap we see today. This is a similar arc as in Web 2: it took 15 years of web browser development for Facebook to be able to launch.

We are dealing with a very young phenomenon and it is not without its issues. The biggest problem is that it will take some time for the users to learn the new technology. Although there are new concepts to be learned, like wallets, and the user experience might never be the same as with centralised online services, Internet users have gone through similar transitions before: learning email, learning smart phones, and learning social media.

Because users are still somewhat illiterate when comes to blockchain technologies they are easily preyed on by scams, both technology and investment. However, this phase will pass over time as users learn. People today are no longer falling for Nigerian prince emails.

Conclusion

It took 10 years for Linux to get from an academic exercise to the mainstream operating system. Then it took another 10 years to become the king of operating systems everywhere. This meant disruption of the existing industrial players (Microsoft, IBM, Sun) but in the end, it led to better services for consumers (Android mobile phones, cloud servers).

Ten years after the launch of Bitcoin, a similar revolution is now happening, as open source is coming to financial services. Public blockchains and decentralised exchanges are at the core of this movement. There is no fundamental reason why they won't succeed. Regulators and the public are concerned; both because of real concerns and sometimes because of the lack of information and mistruths, or sometimes just because of natural resistance to change against a new phenomenon.

The change is needed, though. Even though providing the trading services is a race to the bottom, the race may have unintended consequences for the service users. It is better to build an ecosystem where the service users have a larger say on matters and even the smallest participants can easily work together. Promoting the movement that emphasises transparency and fairness is a great counterweight against these concerns, with less need for regulatory intervention to keep the game fair. This is exactly what decentralised finance will do long term.

Questions or comments? Discuss on Twitter.

Trading Strategy is an algorithmic trading protocol for decentralised markets, enabling automated trading on decentralised exchanges (DEXs). Learn more about algorithmic trading here.

Join our community of traders and developers on Discord.