Developing an algorithmic trading strategy comes with its fair share of challenges, and one of the most critical pitfalls to avoid is overfitting. In this article, we delve into the concept of overfitting and its potential impact on trading performance. Overfitting occurs when a strategy performs exceptionally well on historical data but fails to deliver similar results in real-world trading. We explore the causes of overfitting, including excessive optimisation, limited or biassed data, high complexity, and ignoring transaction costs.

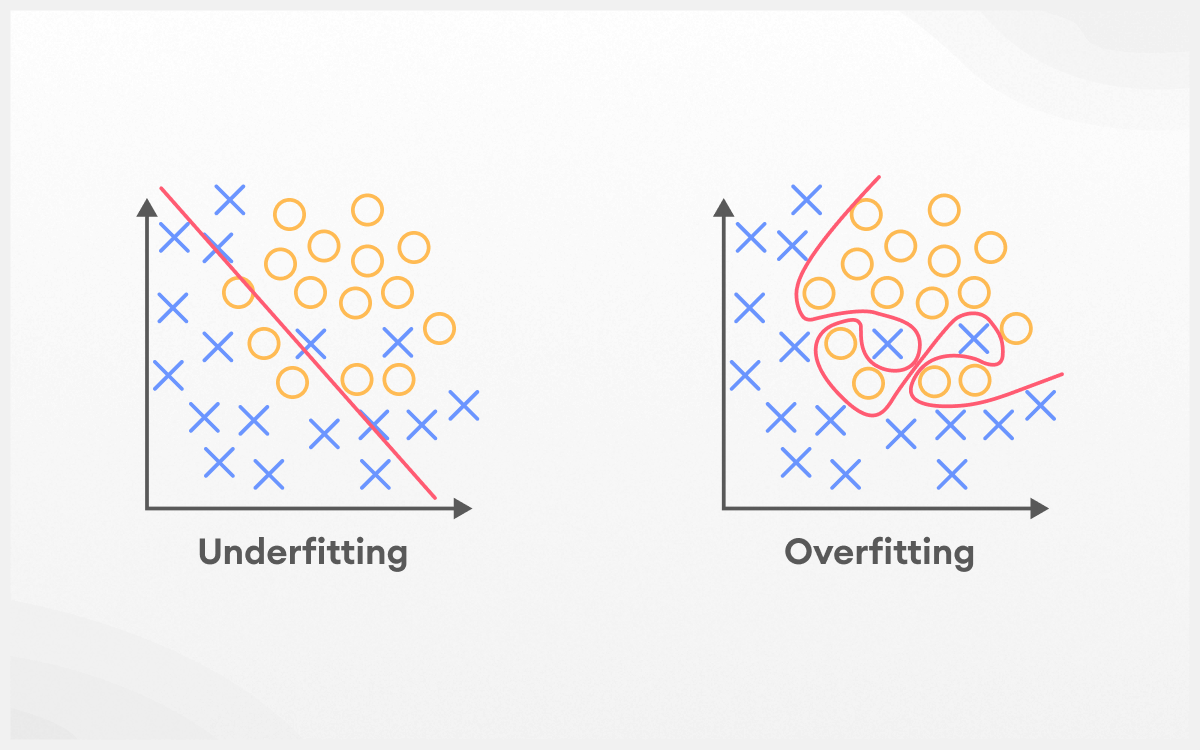

What is overfitting?

Overfitting is a term used to describe the phenomenon where a model performs well on the data it was trained on, but poorly on new data. This is often caused by the model learning the noise in the data rather than the underlying pattern.

In general, overfitting can be avoided by using a larger training set, or by using regularisation techniques such as dropout or weight decay. It is also important to use cross-validation to ensure that the model is not overfitting to the training data.

Specific to algo trading development, once a successful strategy has been identified using backtesting, we should try it on different dates, trading pairs and candle time frames. If results are drastically worse after trying this, the strategy is likely a victim of overfitting.

What causes overfitting?

Causes of overfitting include:

- Excessive optimisation: Fine-tuning an algorithm with too many parameters or constantly tweaking it to achieve optimal results on historical data can lead to overfitting. The algorithm becomes too specialised for the specific data set and fails to perform well on new data.

- Limited or biassed data: Using a small or unrepresentative data sample can cause the algorithm to become overly sensitive to the peculiarities of the data set, leading to overfitting. It is important to use diverse, high-quality, and sufficient data for training.

- High complexity: Using overly complex models with too many variables can result in a model that fits the noise in the data rather than capturing the underlying market trends. Simpler models often generalise better to new data.

- Ignoring transaction costs: In the development stage, it's easy to overlook trading fees, slippage, and other transaction costs. However, these costs can significantly impact live trading performance, leading to a discrepancy between backtested and live results.

How to overcome overfitting?

By using Trading Strategy's backtesting framework, you will automatically avoid the previous point regarding transaction costs, since we allow developers to account for trading fees, price impact, and slippage. Here are some tips to avoid the other causes:

- Use out-of-sample testing: Split your data into training and testing sets. Develop your algorithm on the training set and evaluate its performance on the testing set to gauge its ability to generalise to unseen data.

- Keep it simple: Start with a simpler model and only increase complexity if it significantly improves performance. Occam's razor suggests that simpler models are often better at generalising to new data.

- Monitor performance: Continuously track the performance of your algorithm in live trading and compare it to your backtested results. This can help you identify any potential overfitting and make necessary adjustments.

Quick tip: Once you have found a successful strategy, try it on different trading pairs and candle time frames. If your results are drastically worse after trying this, your strategy is likely a victim of overfitting.

Final thoughts

In conclusion, avoiding overfitting is crucial to the success of any algo trading strategy. By understanding the causes of overfitting and implementing best practices, such as using out-of-sample testing, keeping models simple, and monitoring performance, you can develop a robust and adaptable trading algorithm. Remember, the ultimate goal is to create a strategy that performs consistently well in various market conditions, rather than one that merely excels on historical data. By focusing on these principles and leveraging the powerful tools provided by Trading Strategy's backtesting framework, you can significantly increase the likelihood of developing a successful and profitable algorithmic trading strategy.