In the world of algorithmic trading, the principle of mean reversion has shaped numerous successful strategies. This principle operates on the belief that prices tend to gravitate towards an underlying stable "mean." Whether derived from an asset's historical average or fundamental indicators such as earnings or book value, this “mean” serves as a reference point. Traders who adopt a mean reversion strategy capitalise on price corrections when an asset significantly deviates from its mean. We explore the fundamentals of mean reversion trading, its implementation steps, challenges, and the importance of careful analysis and risk management for successful execution.

What is mean reversion?

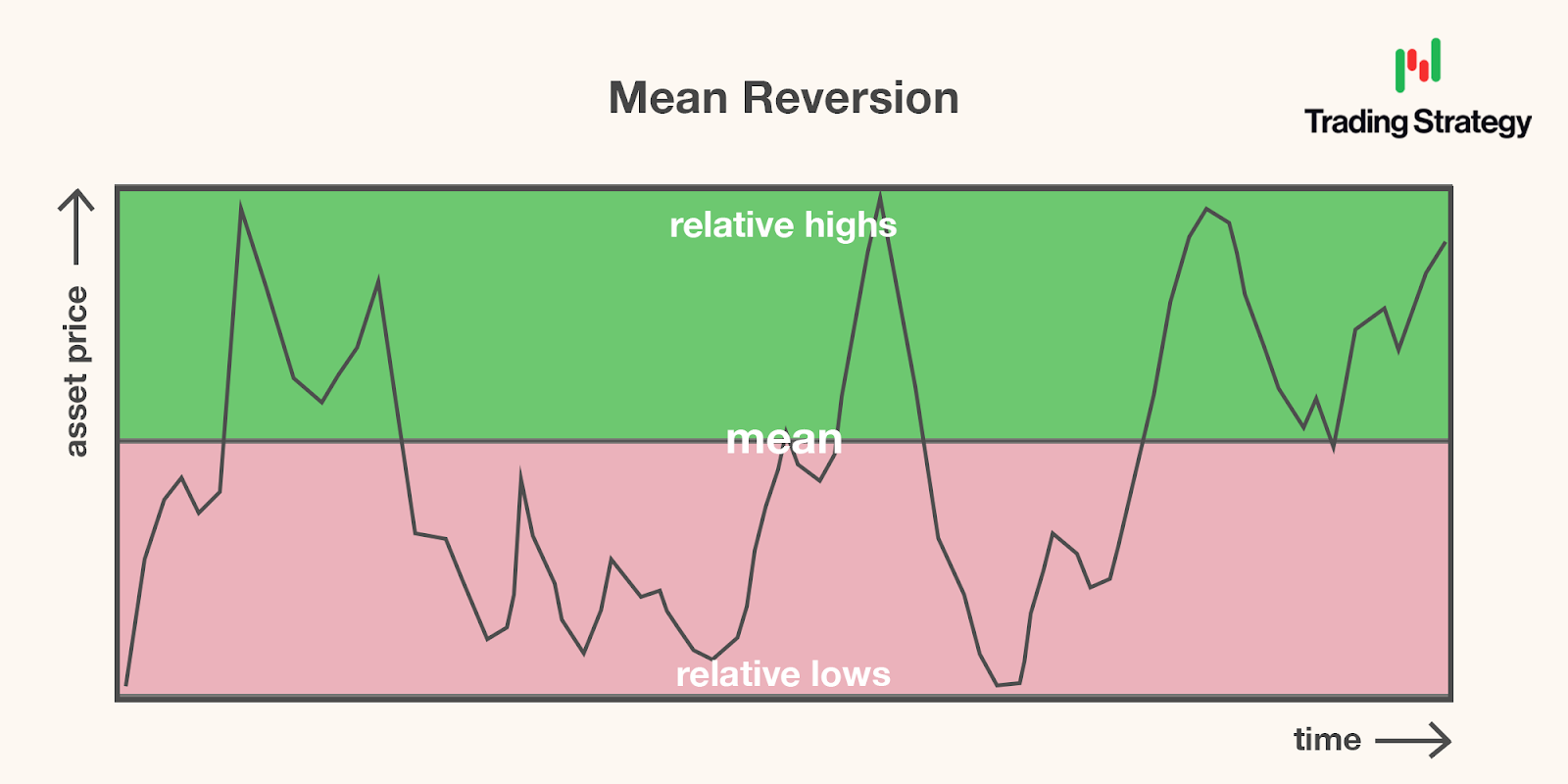

The principle of mean reversion is premised on the assumption that there is an underlying stable "mean" that a price will gravitate towards. The "mean" could be an asset's historical average price, or it could be based on fundamentals like earnings or book value.

Traders employing a mean reversion strategy essentially bet on the price correction of an asset that has significantly deviated from its mean. When an asset's price drifts too far below the mean, it's considered undervalued, indicating a buying opportunity. Conversely, if it drifts too far above the mean, it's seen as overvalued, presenting a selling or shorting opportunity.

How to use a mean reversion trading strategy

A fundamental mean reversion trading strategy might involve the following steps:

- Asset Selection: Traders choose the asset they believe exhibits mean-reverting properties. This could be any financial instrument, token, or asset.

- Defining the Mean: The next step is to determine the "mean." Often, this is a simple or exponential moving average of the asset's price over a specific period.

- Identify Significant Deviations: Traders then identify significant deviations from this mean. This is typically done using statistical measures like standard deviation.

- Generate Trading Signals: When an asset's price significantly deviates from the mean, it generates a trading signal. If the price is above the mean, traders might sell or short the asset. If it's below the mean, they might buy the asset

- Exit Strategy: Finally, an exit strategy is needed to decide when to close the trade. This could be when the price reverts to the mean, reaches a profit target, or triggers a stop loss.

Mean reversion in action

An example of mean reversion can be found here in our documentation, which we have already covered in detail. Bollinger Bands serve as a prime illustration of the mean reversion concept. In this framework, the middle band, which is a moving average, symbolises the 'mean' price over a certain period. The outer bands then represent specific deviations from this mean. When prices reach these outer bands, they are considered to have deviated significantly from the mean, suggesting a potential reversion may be imminent. Note that this example may also fall under the definition of a momentum strategy, since it also uses the RSI indicator in the buy signal.

The benchmark equity curve for this strategy is shown below. The dark green represents the total equity of the strategy over time and the light green represents a simple buy-and-hold for WAVAX. Clearly, the strategy has significantly outperformed the buy-and-hold. Although the final returns are not great at around 7%, the fact that it was able to generate positive returns during a clearly bearish phase in the market is promising.

Challenges and considerations

While mean reversion strategies can be profitable, they aren't without risks. Prices can deviate from their mean for extended periods, or the mean itself can change over time. This is particularly true during periods of significant market upheaval or structural change.

Moreover, transaction costs can significantly impact net returns from mean-reversion strategies due to the potentially high volume of trades. Therefore, these costs must be factored into any trading strategy.

Finally, backtesting and optimisation are crucial before implementing a mean reversion strategy in live markets. Backtesting allows traders to evaluate how the strategy would have performed in the past, providing valuable insights for optimising parameters for profitability and risk management.

Final thoughts

Mean reversion has proven to be a powerful principle in algorithmic trading, offering traders opportunities to capitalise on price corrections. By identifying deviations from the mean and generating precise trading signals, traders can strategically buy or sell assets. However, it's important to approach mean reversion strategies with caution due to risks such as prolonged deviations and changing means. Transaction costs should be factored in, and thorough backtesting and optimization are crucial for successful implementation. By mastering the art of mean reversion and effectively managing risks, algorithmic traders can leverage its potential to improve their trading strategy and overall analysis.