Backtesting is a critical component of any trading strategy, allowing traders to evaluate the performance of their trading algorithm using historical data. Traditional backtesting approaches rely on statistical methods to analyse past market behaviour and estimate the expected outcomes of a trading strategy. However, these methods may not capture the complexity and uncertainty inherent in financial and cryptocurrency markets.

One solution to this problem is to use Monte Carlo simulations for backtesting. We explore why the Monte Carlo simulation is a powerful tool for backtesting and how it can be used to help you determine the true performance of your algorithmic trading strategy.

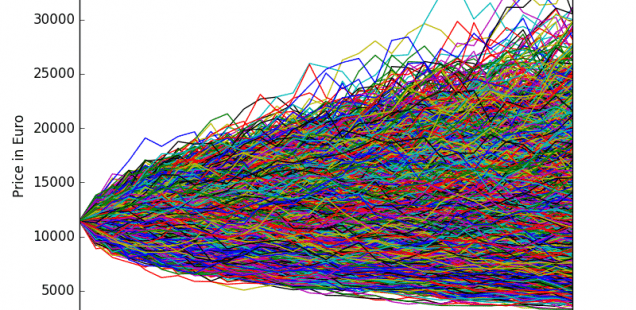

What is a Monte Carlo simulation?

Monte Carlo simulation is a statistical technique used to model complex systems and simulate their behaviour, where computational algorithms are used to estimate the probability of an uncertain event involving random variables. It is named after the famous Monte Carlo casino, where roulette players can make a series of bets and see how the game unfolds over time.

The method relies on repeated random sampling to determine the likelihood of the event. This involves simulating the event with random inputs numerous times to obtain an estimation. For example, a strategy developer would run a series of backtests on random samples from historical market data to understand how it would perform at different times and during different market fluctuations.

The key advantage of Monte Carlo simulation is its ability to model the complexity and uncertainty of financial markets without having to make real trades. Rather than assuming that market behaviour follows a fixed distribution, Monte Carlo simulation allows traders to help detect luck and determine appropriate drawdown measures beyond what a simple backtest can provide. By employing reshuffle and resample techniques, traders can simulate various equity curves with alternative trade sequences, which can offer insights into potential outcomes.

This approach provides a more accurate estimate of the performance of a trading strategy, as it takes into account the inherent uncertainty and randomness of financial markets.

Why use a Monte Carlo simulation for backtesting?

There are several reasons the Monte Carlo simulation is a superior technique for backtesting:

- Captures market complexity: Traditional backtesting methods often rely on simplistic assumptions about market behaviour, such as assuming that returns follow a normal distribution. This approach fails to capture the complex and dynamic nature of financial markets. Monte Carlo simulation, on the other hand, allows traders to model the full complexity of market behaviour, including volatility, correlation, and regime changes.

- Generates more realistic results: Traditional backtesting methods can produce misleading results if the assumptions underlying the model are incorrect. Monte Carlo simulation, by contrast, generates a range of possible outcomes, providing a more realistic estimate of the performance of a trading strategy under different market conditions.

- Incorporates uncertainty: Financial markets are inherently uncertain, and traditional backtesting methods often fail to account for this uncertainty. Monte Carlo simulation, on the other hand, explicitly models uncertainty and generates a range of possible outcomes, allowing traders to assess the risk associated with their trading strategies.

- Provides a basis for optimization: Monte Carlo simulation can be used to evaluate the performance of different trading strategies under different market conditions. By comparing the results of different simulations, traders can identify the most effective strategies and optimise their trading approach.

How effective is a Monte Carlo simulation for backtesting?

The utilisation of Monte Carlo simulation analysis is a valuable technique for algorithmic traders as it allows them to evaluate their trading strategy’s performance across wider market conditions. These Monte Carlo methods are widely used among traders to distinguish between luck and accurate drawdown measures beyond what a basic backtest can reveal. These methods involve reshuffling and resampling, enabling traders to simulate a range of equity curves with different trade sequences and gain insight into potential outcomes.

When it comes to quantitative trading, Monte Carlo simulations are considered one of the most favoured tools to incorporate into an algorithmic trading arsenal. More advanced traders may even adjust variables such as the probability density function or random number generator to refine their MC selections.