Liquidity analysis#

This is an example how to analyse Automated Market Market liquidity on a blockchain. It is similar of order book depth analysis on centralised exchanges.

We will

Download pair and exchange map (“the trading universe”)

Plot a liquidity of a single trading pair on SushiSwap

Compare the historical liquidity of all pairs on SushiSwap and Uniswap v2

Calculate the slippage for a hypotethical trade that would have happened at a specific timepoint

About liquidity data collection on AMM exchanges#

Trading Strategy maintains the data of Uniswap v2 style, x*y = k bonding curve, liquidity in a similar format as it maintains OHLC price data. In more traditional finance, the equivalent analysis would be an order book depth - how much you can buy or sell and how much it would move the price.

For each time bucket you get the available liquidity

At open (start of the time bucket period)

At close (end of the time bucket period)

At peak (high of the time bucket period)

At bottom (low of the time bucket period)

The liquidity is expressed as the US dollar depth of the one side of the pool. E.g. the liquidity of a pool with 50 USDC and 0.001 ETH would be 50 USD.

There is also something very swap liquidity pool specific measurements

Added and removed liquidity, as volume and as number of transactions

The liquidity data can be very effectively used to analyse or predict the trading fees of a swap.

[ ]:

Getting started#

First, let’s create Trading Strategy dataset client.

[1]:

from tradingstrategy.client import Client

client = Client.create_jupyter_client()

Started Trading Strategy in Jupyter notebook environment, configuration is stored in /Users/moo/.tradingstrategy

Fetching datasets#

Get the map of exchanges and pairs we are working on

[2]:

from pyarrow import Table

from tradingstrategy.exchange import ExchangeUniverse

from tradingstrategy.pair import PandasPairUniverse

from tradingstrategy.timebucket import TimeBucket

from tradingstrategy.liquidity import GroupedLiquidityUniverse

# Exchange map data is so small it does not need any decompression

exchange_universe: ExchangeUniverse = client.fetch_exchange_universe()

# Fetch all trading pairs across all exchanges

pair_table: Table = client.fetch_pair_universe()

pair_universe = PandasPairUniverse(pair_table.to_pandas())

# GroupedLiquidityUniverse is a helper class that

# encapsulates Pandas grouped array

liquidity_table: Table = client.fetch_all_liquidity_samples(TimeBucket.d1)

liquidity_universe = GroupedLiquidityUniverse(liquidity_table.to_pandas())

Single pair liquidity#

Here we first narrow down our data to single trading

[3]:

from tradingstrategy.chain import ChainId

from tradingstrategy.pair import DEXPair

# Filter down to pairs that only trade on Sushiswap

sushi_swap = exchange_universe.get_by_chain_and_slug(ChainId.ethereum, "sushi")

pair: DEXPair = pair_universe.get_one_pair_from_pandas_universe(

sushi_swap.exchange_id,

"WETH",

"USDC")

eth_usdc_liquidity = liquidity_universe.get_liquidity_samples_by_pair(pair.pair_id)

Let’s create a table to explore the liquidity for a specific month

[4]:

import datetime

start = datetime.datetime(2020, 10, 1)

end = datetime.datetime(2020, 11, 1)

df = eth_usdc_liquidity[["open", "high", "low", "close"]]

def format(x):

return "${:.1f}M".format(x / 1_000_000)

df = df.applymap(format)

df[start:end]

[4]:

| open | high | low | close | |

|---|---|---|---|---|

| timestamp | ||||

| 2020-10-01 | $24.1M | $28.3M | $13.2M | $14.6M |

| 2020-10-02 | $14.5M | $23.2M | $14.5M | $23.1M |

| 2020-10-03 | $23.1M | $23.4M | $22.3M | $22.7M |

| 2020-10-04 | $22.7M | $22.8M | $22.1M | $22.3M |

| 2020-10-05 | $22.3M | $22.4M | $16.9M | $17.1M |

| 2020-10-06 | $17.1M | $17.7M | $16.2M | $16.7M |

| 2020-10-07 | $16.7M | $16.7M | $15.1M | $16.3M |

| 2020-10-08 | $16.4M | $16.8M | $14.7M | $15.0M |

| 2020-10-09 | $15.0M | $19.5M | $15.0M | $19.4M |

| 2020-10-10 | $19.4M | $20.4M | $19.4M | $19.7M |

| 2020-10-11 | $19.7M | $20.0M | $19.5M | $19.6M |

| 2020-10-12 | $19.6M | $20.3M | $19.3M | $19.5M |

| 2020-10-13 | $19.5M | $20.3M | $18.0M | $18.3M |

| 2020-10-14 | $18.3M | $19.1M | $18.3M | $19.1M |

| 2020-10-15 | $19.1M | $19.8M | $19.0M | $19.7M |

| 2020-10-16 | $19.7M | $19.9M | $19.4M | $19.6M |

| 2020-10-17 | $19.6M | $19.8M | $19.2M | $19.8M |

| 2020-10-18 | $19.8M | $20.9M | $19.8M | $20.9M |

| 2020-10-19 | $20.9M | $21.5M | $20.8M | $20.8M |

| 2020-10-20 | $20.8M | $20.8M | $20.0M | $20.0M |

| 2020-10-21 | $20.0M | $20.8M | $20.0M | $20.6M |

| 2020-10-22 | $20.7M | $21.2M | $20.0M | $20.8M |

| 2020-10-23 | $20.8M | $21.0M | $11.6M | $15.4M |

| 2020-10-24 | $15.4M | $16.6M | $15.4M | $16.5M |

| 2020-10-25 | $16.5M | $16.6M | $16.4M | $16.4M |

| 2020-10-26 | $16.4M | $19.5M | $16.3M | $19.4M |

| 2020-10-27 | $19.5M | $20.1M | $19.2M | $19.8M |

| 2020-10-28 | $19.7M | $19.9M | $18.2M | $18.4M |

| 2020-10-29 | $18.4M | $18.5M | $17.9M | $18.0M |

| 2020-10-30 | $18.0M | $18.0M | $17.7M | $17.9M |

| 2020-10-31 | $17.9M | $18.2M | $17.8M | $18.1M |

| 2020-11-01 | $18.1M | $18.3M | $18.1M | $18.3M |

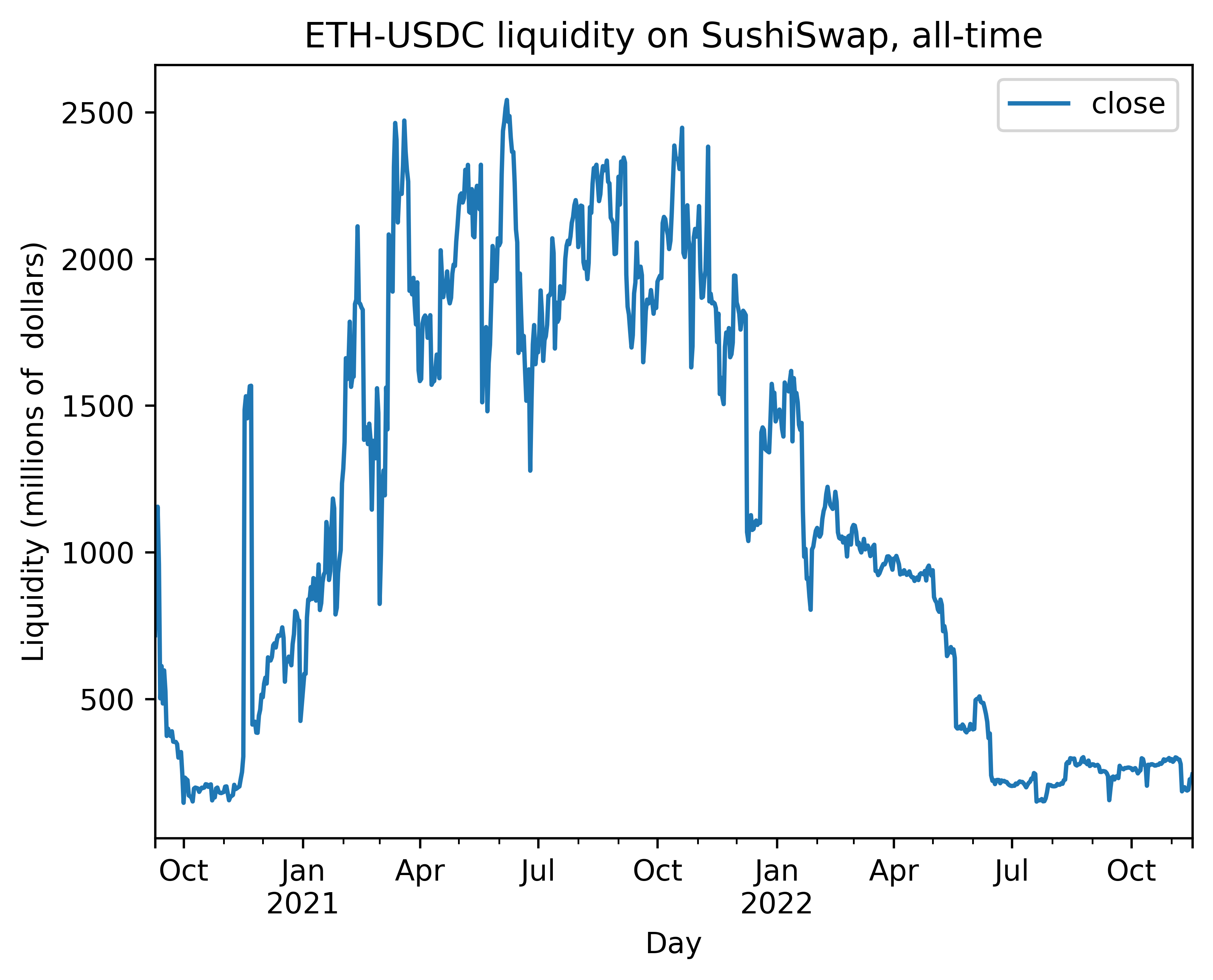

Now, let’s plot how the liquidity has developed over the time. For OHLC liquidity values, we use high (peak) liquidity.

We also cut off the launch of the SushiSwap away from the time series, because the launch date was special due to SushiSwap’s vampire attack on Uniswap liquidity (100x more liquidity available).

[5]:

df = eth_usdc_liquidity[["close"]]

# Convert to millions

df["close"] = df["close"] / 1_000_00

/var/folders/12/pbc59svn70q_9dfz1kjl3zww0000gn/T/ipykernel_82533/112040287.py:4: SettingWithCopyWarning:

A value is trying to be set on a copy of a slice from a DataFrame.

Try using .loc[row_indexer,col_indexer] = value instead

See the caveats in the documentation: https://pandas.pydata.org/pandas-docs/stable/user_guide/indexing.html#returning-a-view-versus-a-copy

df["close"] = df["close"] / 1_000_00

Let’s plot the liquidity using Pandas internal plotting functions for Jupyter notebook

[6]:

from tradingstrategy.frameworks.matplotlib import render_figure_in_docs

axes_subplot = df.plot(title="ETH-USDC liquidity on SushiSwap, all-time")

axes_subplot.set_xlabel("Day")

axes_subplot.set_ylabel("Liquidity (millions of dollars)")

axes_subplot

[6]:

<AxesSubplot: title={'center': 'ETH-USDC liquidity on SushiSwap, all-time'}, xlabel='Day', ylabel='Liquidity (millions of dollars)'>

Comparing liquidity across exchanges#

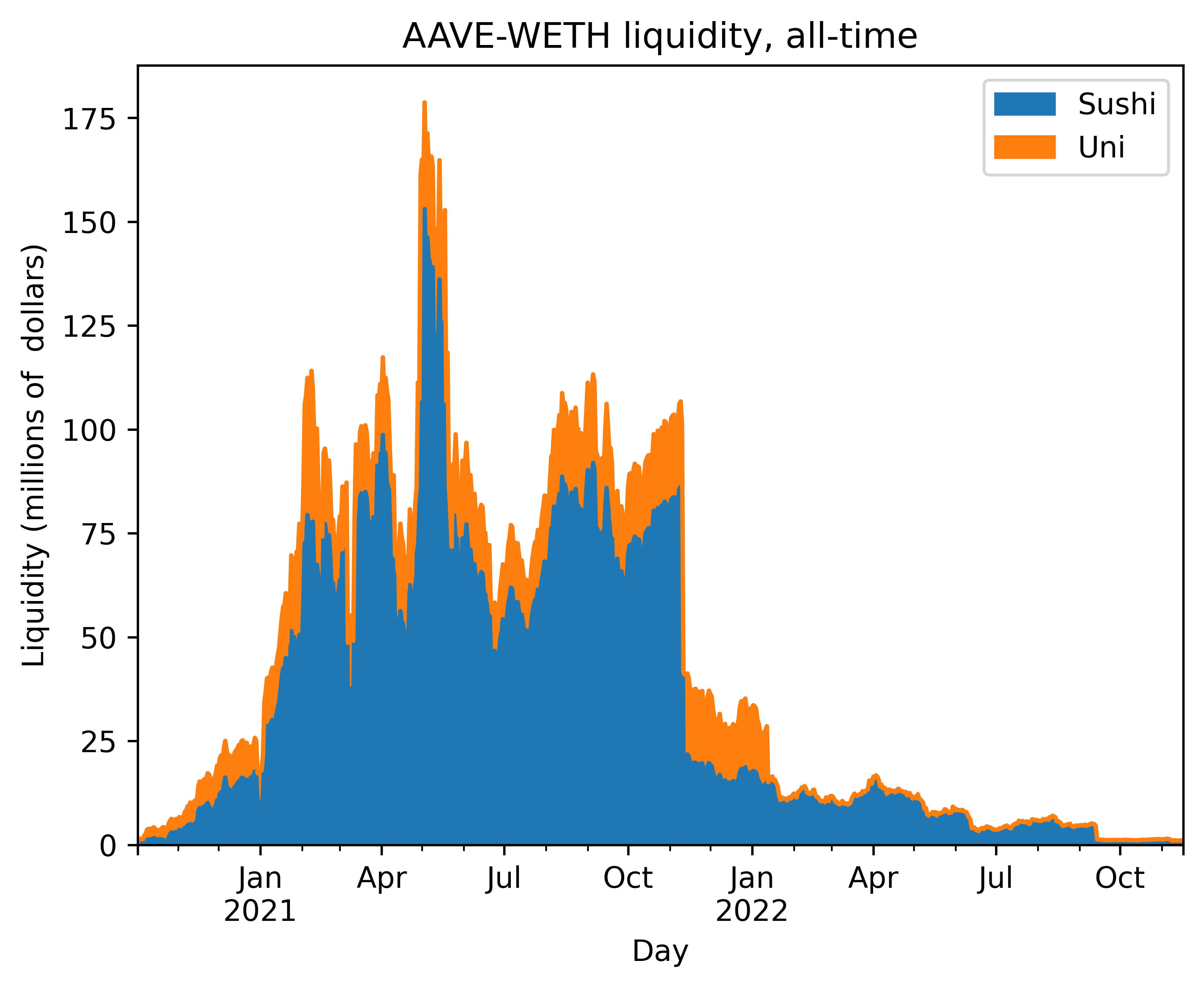

In this example, we compare the liquidity across Uniswap and Sushiswap for WETH-AAVE pair. We see that AAVE traders prefer Sushiswap.

[7]:

import pandas as pd

uniswap_v2 = exchange_universe.get_by_chain_and_slug(ChainId.ethereum, "uniswap-v2")

sushi_swap = exchange_universe.get_by_chain_and_slug(ChainId.ethereum, "sushi")

pair1: DEXPair = pair_universe.get_one_pair_from_pandas_universe(

sushi_swap.exchange_id,

"AAVE",

"WETH")

# Uniswap has fake listings for AAVE-WETH, and

# pick_by_highest_vol=True will work around this by

# using the highest volume pair of the same name.

# Usually the real pair has the highest volume and

# scam tokens have ~0 volume.

pair2: DEXPair = pair_universe.get_one_pair_from_pandas_universe(

uniswap_v2.exchange_id,

"AAVE",

"WETH",

pick_by_highest_vol=True)

liq1 = liquidity_universe.get_liquidity_samples_by_pair(pair1.pair_id)

liq2 = liquidity_universe.get_liquidity_samples_by_pair(pair2.pair_id)

Now construct a chart that shows the both liquidities, stacked.

[8]:

# Scale liquidity candles on the both series to $1M

sushi = liq1[["close"]] / 1_000_000

uni = liq2[["close"]] / 1_000_000

# Merge using timestamp index

df = pd.merge_ordered(sushi, uni, fill_method="ffill", on="timestamp")

df = df.set_index("timestamp")

df = df.rename(columns={"close_x": "Sushi", "close_y": "Uni"})

axes_subplot = df.plot.area(title="AAVE-WETH liquidity, all-time")

axes_subplot.set_xlabel("Day")

axes_subplot.set_ylabel("Liquidity (millions of dollars)")

axes_subplot

[8]:

<AxesSubplot: title={'center': 'AAVE-WETH liquidity, all-time'}, xlabel='Day', ylabel='Liquidity (millions of dollars)'>